Before applying for a bank account, credit card, loan, or financial app, it is important to read the financial terms carefully.

Many beginners focus only on the main offer. They may look at rewards, bonuses, fast approval, low monthly payments, or easy account opening.

However, the most important details are often found in the terms, disclosures, fee schedule, and fine print.

Financial terms explain how the product works, what it may cost, what rules apply, and what responsibilities you have after signing up.

This guide explains how beginners can read financial terms before applying.

Why Financial Terms Matter

Financial terms matter because they can affect your money, credit, fees, payments, and long-term financial situation.

A product may look simple in an advertisement, but the full terms may include costs or requirements that are easy to miss.

For example, a bank account may advertise no monthly fee, but the fee may only be waived if you meet certain requirements.

A credit card may offer rewards, but it may also have a high APR, annual fee, or spending requirement.

A loan may show a low monthly payment, but the full repayment cost may be much higher over time.

Reading financial terms can help you:

- Understand the real cost

- Avoid surprise fees

- Compare products more clearly

- Know your responsibilities

- Avoid products that do not fit your needs

- Protect your credit

- Make better financial decisions

The goal is not to become a financial expert.

The goal is to understand the basic rules before you apply.

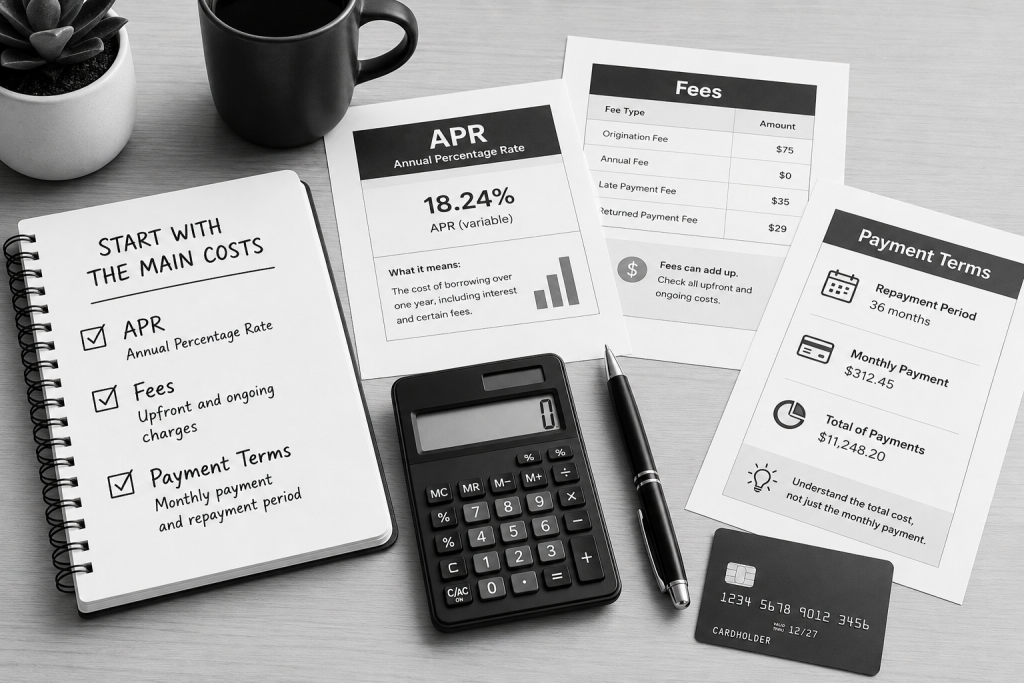

Start With the Main Costs

When reading financial terms, start with the main costs.

Costs are one of the most important parts of any financial product.

For a bank account, costs may include monthly maintenance fees, overdraft fees, ATM fees, wire transfer fees, paper statement fees, or account closing fees.

For a credit card, costs may include annual fees, APR, late payment fees, balance transfer fees, cash advance fees, and foreign transaction fees.

For a loan, costs may include interest, APR, origination fees, late fees, prepayment penalties, and total repayment cost.

For a financial app, costs may include monthly subscription fees, premium plan fees, transfer fees, or service fees.

Before applying, ask:

- What fees can I be charged?

- When do the fees apply?

- Can any fees be avoided?

- Is there a monthly or annual cost?

- What is the total cost over time?

A product that looks free may still have fees in certain situations.

Understand APR

APR stands for Annual Percentage Rate.

APR is one of the most important terms for credit cards and loans.

For credit cards, APR usually tells you how much interest may apply if you carry a balance, take a cash advance, or use certain card features.

For loans, APR can help show the yearly cost of borrowing, including the interest rate and certain fees.

A lower APR usually means lower borrowing costs, but APR is not the only detail to review.

You should also check the repayment term, fees, monthly payment, and total cost.

For credit cards, pay attention to different types of APR, such as:

- Purchase APR

- Balance transfer APR

- Cash advance APR

- Penalty APR

- Introductory APR

An introductory APR may only last for a limited time.

After the promotional period ends, the regular APR may apply.

Always check when the introductory rate ends and what the regular APR will be.

Check Fees Carefully

Fees can make a financial product more expensive than expected.

Some fees are obvious, while others are easy to miss.

Common fees include:

- Monthly maintenance fees

- Annual fees

- Late payment fees

- Overdraft fees

- ATM fees

- Foreign transaction fees

- Balance transfer fees

- Cash advance fees

- Origination fees

- Prepayment penalties

- Returned payment fees

- Subscription fees

- Account closing fees

Not every product has every fee.

The key is to read the fee schedule carefully.

Ask yourself:

- Which fees are most likely to affect me?

- Can I avoid these fees?

- Are the fees reasonable compared with other products?

- Do the benefits justify the fees?

For beginners, simple products with fewer fees are often easier to manage.

Review Payment Terms

Payment terms explain when and how you must pay.

This is especially important for credit cards and loans.

For credit cards, review:

- Payment due date

- Minimum payment

- Statement balance

- Grace period

- Late payment rules

- Penalty APR

- Interest charges

- Returned payment rules

For loans, review:

- Monthly payment amount

- Payment due date

- Loan term

- Repayment schedule

- Total repayment cost

- Late payment rules

- Prepayment rules

- Automatic payment options

A low monthly payment may look attractive, but it can sometimes mean a longer repayment period.

A longer repayment period may increase the total amount paid over time.

Before applying, make sure the payment fits your budget.

Look for Minimum Requirements

Some financial products have minimum requirements.

Bank accounts may require a minimum opening deposit, minimum balance, direct deposit, or a certain number of monthly transactions.

Credit cards may require certain credit history, income, identity verification, or approval standards.

Loans may require income verification, employment information, credit review, collateral, or a minimum loan amount.

Financial apps may require a linked bank account, personal information, identity verification, or a paid subscription after a free trial.

Before applying, check whether you can meet the requirements.

If you cannot meet the requirements, the product may not be a good fit.

Understand Rewards and Benefits

Rewards and benefits can be useful, but they should be reviewed carefully.

Credit cards may offer cash back, points, miles, sign-up bonuses, travel benefits, purchase protection, or other rewards.

Bank accounts may offer cash bonuses, higher savings rates, no monthly fees, or ATM reimbursements.

Financial apps may offer budgeting tools, savings tools, account alerts, or spending insights.

Before choosing based on benefits, ask:

- What do I need to do to earn the benefit?

- Are there limits?

- Does the benefit expire?

- Are there fees that reduce the value?

- Do I need to spend money to earn it?

- Does the benefit fit my real habits?

A reward is not helpful if it encourages unnecessary spending or comes with high costs.

Check Limits and Restrictions

Financial products often have limits and restrictions.

These details may affect how useful the product is.

A savings account may limit withdrawals or transfers.

A checking account may limit free ATM use.

A credit card may limit rewards categories, bonus earnings, balance transfers, or cash advances.

A loan may restrict how funds can be used.

A financial app may limit free features, transfer speed, account connections, or customer support.

Check for:

- Spending limits

- Withdrawal limits

- Transfer limits

- Rewards limits

- Account balance limits

- Loan use restrictions

- Eligibility restrictions

- Geographic restrictions

- Promotional offer limits

A product may still be useful, but you should understand its limits before applying.

Review Cancellation Rules

Cancellation rules are important because you may want to close an account, cancel an app, pay off a loan early, or stop using a product later.

Before applying, check:

- Can I cancel easily?

- Are there cancellation fees?

- Is there an account closing fee?

- Do I need to give notice?

- Can I pay off the loan early?

- Is there a prepayment penalty?

- What happens to rewards if I close the account?

- What happens to my data if I delete the app?

Some products are easy to cancel, while others may have more rules.

Understanding cancellation terms can help you avoid problems later.

Pay Attention to Security and Privacy

Security and privacy are especially important for online accounts, banking apps, budgeting apps, and financial tools.

Before applying or signing up, review how the company protects your account and information.

Look for:

- Two-factor authentication

- Account alerts

- Secure login

- Fraud monitoring

- Card lock features

- Privacy policy

- Data-sharing rules

- Customer support

- Official website and app store links

Be careful with unknown websites, unclear apps, or offers that ask for sensitive information without explaining how it is used.

A financial product should be clear about how it protects your money and personal information.

Read the Fine Print Slowly

The fine print may feel boring, but it often contains important details.

You do not need to understand every legal phrase perfectly, but you should slow down and look for key information.

Focus on:

- Fees

- APR

- Interest rates

- Payment rules

- Due dates

- Requirements

- Limits

- Rewards rules

- Cancellation terms

- Privacy and security

- Customer support

- Dispute rules

If something is unclear, search the company’s help center or contact customer support before applying.

Do not rely only on the headline offer.

The fine print explains how the product really works.

Compare Terms With Other Products

Reading terms becomes easier when you compare more than one product.

If you only read one offer, you may not know whether the fees or APR are reasonable.

Try comparing at least three options when possible.

Create a simple comparison list with:

- Product name

- Main purpose

- Monthly fee

- Annual fee

- APR or interest rate

- Requirements

- Main benefits

- Main risks

- Cancellation rules

- Customer support

This helps you see which option is clearer, cheaper, and more useful for your situation.

A product with simple terms may be better for beginners than a complicated product with many conditions.

Common Beginner Mistakes

One common mistake is applying before reading the full terms.

Another mistake is focusing only on rewards, bonuses, or fast approval.

Some beginners ignore APR because they plan to pay on time, but unexpected situations can happen.

Others ignore fees because the main advertisement says the product is simple or free.

Some people do not check requirements and later realize they cannot meet them.

Another mistake is not reading cancellation rules before signing up for an app or financial service.

Beginners may also compare products only by monthly payment instead of total cost.

Reading the terms before applying can help avoid these mistakes.

Simple Checklist Before Applying

Before applying for a financial product, ask yourself:

- What is this product for?

- What fees apply?

- What is the APR or interest rate?

- What payment rules apply?

- Can I meet the requirements?

- Are there limits or restrictions?

- Are the rewards useful for me?

- What happens if I cancel?

- How is my information protected?

- Does this product fit my real financial needs?

If you cannot answer these questions, keep reviewing before applying.

Final Thoughts

Reading financial terms before applying is one of the best habits beginners can build.

Financial products can be useful, but they can also include fees, APR, requirements, limits, and rules that are easy to miss.

Before opening a bank account, applying for a credit card, accepting a loan, or signing up for a financial app, take time to review the terms carefully.

Start with costs, APR, fees, payment rules, requirements, benefits, limits, cancellation terms, and security.

A product that is clear, affordable, useful, and easy to understand is usually better than one that only looks attractive in advertising.

Disclaimer

The information in this article is for educational purposes only and should not be considered financial, legal, tax, credit, loan, or investment advice. Financial terms, fees, APRs, interest rates, payment rules, rewards, requirements, cancellation policies, and provider terms may change over time. Always review the official terms and disclosures from the financial institution, lender, card issuer, or service provider before applying for or using any financial product. If you have questions about your personal financial situation, consider speaking with a qualified professional.

Leave a Reply