Credit card reviews can be helpful when you are trying to compare different card options.

A review may explain fees, APR, rewards, credit requirements, benefits, risks, and payment terms.

However, beginners should not choose a credit card only because a review sounds positive.

A good credit card review should help you understand both the benefits and the costs.

This guide explains what beginners should look for when reading a credit card review.

Why Credit Card Reviews Matter

Credit card reviews matter because credit cards can affect your budget, credit history, fees, and borrowing costs.

A credit card may offer cash back, points, travel rewards, sign-up bonuses, purchase protection, or no annual fee.

But credit cards may also come with APR, late fees, annual fees, penalty charges, and the risk of carrying debt.

A good review should explain:

- What the card is best for

- Who the card may fit

- What fees apply

- What APR applies

- How rewards work

- What credit level may be needed

- What benefits are included

- What risks exist

- What payment rules apply

- What limitations you should know

For beginners, the goal is to choose a card that is simple, affordable, and easy to manage.

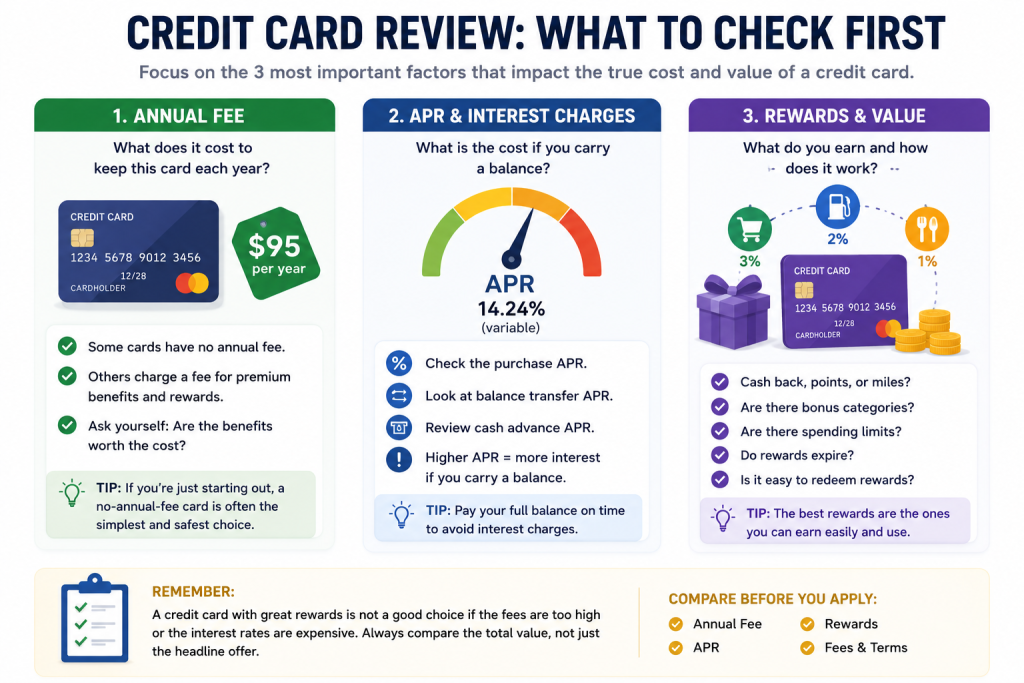

Check the Annual Fee

The annual fee is one of the first things to check in a credit card review.

An annual fee is a yearly cost charged for having the card.

Some credit cards have no annual fee.

Other cards may charge an annual fee in exchange for rewards, travel benefits, credits, insurance protections, or premium features.

Before choosing a card with an annual fee, ask:

- How much is the annual fee?

- Are the benefits worth the cost?

- Will I actually use the benefits?

- Is there a no-annual-fee option?

- Does the card fit my spending habits?

For beginners, a no-annual-fee card is often easier to manage.

A card with an annual fee may be useful for some people, but only if the benefits clearly outweigh the cost.

Understand APR and Interest Charges

APR stands for Annual Percentage Rate.

For credit cards, APR usually matters if you carry a balance from month to month.

If you pay your full statement balance by the due date, you may avoid interest on purchases, depending on the card terms.

If you carry a balance, interest can become expensive.

A credit card review should explain:

- Purchase APR

- Balance transfer APR

- Cash advance APR

- Penalty APR

- Introductory APR

- Regular APR after promotion

- Whether the APR is variable

- How interest may apply

Beginners should be careful with cards that have high APRs.

Even strong rewards may not be worth it if interest charges build up.

A credit card should not be treated as extra income.

It is borrowed money that must be repaid.

Review Rewards Carefully

Rewards can make a credit card attractive, but they should be reviewed carefully.

Common rewards may include:

- Cash back

- Points

- Travel miles

- Statement credits

- Category bonuses

- Rotating rewards

- Flat-rate rewards

- Store rewards

A review should explain how rewards are earned and how they can be redeemed.

Important questions include:

- How much do you earn per dollar?

- Are rewards limited to certain categories?

- Do categories change?

- Are there spending caps?

- Do rewards expire?

- Can rewards be redeemed easily?

- Are there fees that reduce the value?

- Do you need to spend more to earn rewards?

Rewards are helpful only if they match your normal spending.

If a card encourages you to spend more than usual, the rewards may not be worth it.

Look at Sign-Up Bonuses

Some credit cards offer sign-up bonuses.

A sign-up bonus may give cash back, points, miles, or statement credits after you spend a certain amount within a certain time.

A review should clearly explain the bonus requirements.

Check:

- How much is the bonus?

- How much spending is required?

- How long do you have to meet the requirement?

- What purchases count?

- When is the bonus paid?

- Are there restrictions?

- Does the spending requirement fit your normal budget?

A sign-up bonus can be useful, but it should not encourage unnecessary spending.

If you need to spend more than you normally would, the bonus may not be a good reason to apply.

Check Credit Requirements

Credit card reviews often mention who the card may be best for.

Some cards are designed for beginners.

Some are designed for people with fair credit, good credit, or excellent credit.

Some are secured credit cards, which may require a refundable security deposit.

Before applying, check whether the card may fit your credit situation.

A review may discuss:

- Credit score range

- Credit history expectations

- Income review

- Approval difficulty

- Secured card requirements

- Student card options

- Beginner-friendly options

- Prequalification availability

Approval is never guaranteed.

But understanding the likely requirements can help you avoid applying for cards that may not fit your situation.

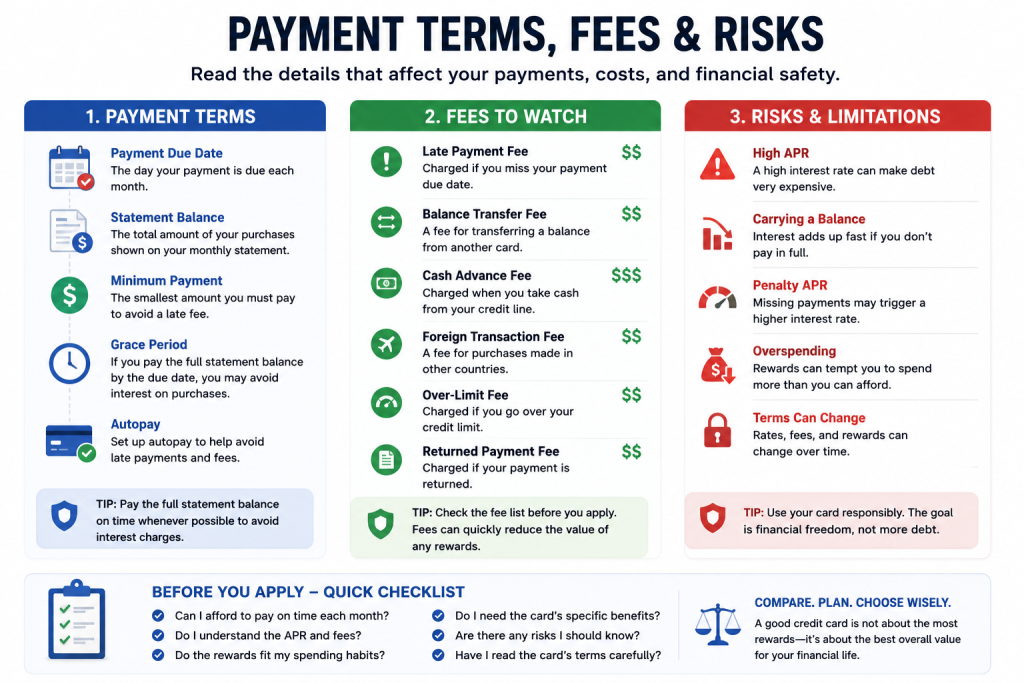

Review Fees and Penalties

Fees can make a credit card more expensive.

A good credit card review should explain more than just the annual fee.

Common fees may include:

- Late payment fee

- Balance transfer fee

- Cash advance fee

- Foreign transaction fee

- Returned payment fee

- Over-limit fee

- Penalty APR

- Replacement card fee

Ask:

- What fees apply?

- When do these fees happen?

- Can the fees be avoided?

- Are the fees common compared with similar cards?

- Could my habits trigger these fees?

For beginners, cards with fewer fees and clearer rules are usually easier to manage.

Understand Payment Terms

Payment terms explain how and when you must pay.

This is one of the most important parts of using a credit card responsibly.

A review should explain or remind readers to check:

- Payment due date

- Statement balance

- Minimum payment

- Grace period

- Late payment rules

- Interest charges

- Autopay options

- Returned payment rules

- Penalty APR

The minimum payment is not the same as paying the full balance.

If you only make the minimum payment, you may carry debt and pay interest.

For beginners, the safest habit is usually to pay the full statement balance on time whenever possible.

Compare Benefits and Protections

Credit cards may include extra benefits.

These benefits can vary widely by card.

Common benefits may include:

- Fraud protection

- Purchase protection

- Extended warranty

- Rental car coverage

- Travel insurance

- Trip delay coverage

- Lost luggage coverage

- Cell phone protection

- Credit score tools

- Account alerts

- Card lock features

A review should explain which benefits are included and whether they are useful.

However, benefits may have limits, conditions, and exclusions.

Always review the official card guide or benefits terms before relying on any protection.

Look at Risks and Limitations

A balanced credit card review should include risks and limitations.

A card may have good rewards but a high APR.

A card may have a bonus but require high spending.

A card may have travel benefits but charge an annual fee.

A card may have rotating categories that require activation.

A secured card may require a deposit.

A store card may have limited use or high APR.

Common risks include:

- Carrying a balance

- Paying interest

- Missing payments

- Overspending for rewards

- Ignoring fees

- Applying for cards that do not fit

- Using cash advances

- Not understanding promotional APR terms

A good review should help you understand what could go wrong, not only what looks attractive.

Compare the Card With Alternatives

One credit card review is not enough.

Beginners should compare multiple cards before applying.

Compare:

- Annual fee

- APR

- Rewards structure

- Sign-up bonus

- Credit requirements

- Foreign transaction fees

- Late fees

- Balance transfer terms

- Cash advance terms

- Benefits

- Customer support

- Ease of use

- Limitations

A card that looks good alone may not be the best option when compared with alternatives.

Simple cards with low fees and clear terms are often better for beginners.

Read the Official Terms

Reviews are useful, but the official terms are more important.

Credit card terms can change.

A review may become outdated, or it may not include every detail.

Before applying, review the official card disclosures from the card issuer.

Check:

- Rates and fees

- Rewards terms

- Bonus requirements

- Payment rules

- APR details

- Penalty rules

- Benefit limits

- Eligibility requirements

- Privacy policy

- Account agreement

Do not rely only on summaries.

The official terms explain the real rules.

Common Beginner Mistakes

One common mistake is choosing a card only because it has rewards.

Rewards are not helpful if the card leads to interest charges or overspending.

Another mistake is ignoring APR because you plan to pay in full.

Paying in full is a good goal, but unexpected situations can happen.

Some beginners apply for cards with annual fees without knowing whether the benefits are worth it.

Others chase sign-up bonuses and spend more than planned.

Another mistake is making only the minimum payment.

Some people also ignore foreign transaction fees, balance transfer fees, or cash advance fees.

A credit card review should help beginners avoid these mistakes.

Simple Checklist Before Applying

Before applying for a credit card, ask:

- Is there an annual fee?

- What is the APR?

- Can I pay the full balance on time?

- How do rewards work?

- Do rewards fit my normal spending?

- Is there a sign-up bonus?

- Can I meet the bonus requirement without overspending?

- What credit level may be needed?

- What fees apply?

- What happens if I miss a payment?

- Are benefits useful to me?

- What are the risks?

- Did I read the official terms?

If you cannot answer these questions, take more time before applying.

Final Thoughts

Credit card reviews can help beginners compare cards more clearly.

A good review should explain annual fees, APR, rewards, bonuses, credit requirements, payment terms, benefits, fees, risks, and limitations.

Do not choose a credit card only because of rewards or advertising.

Choose a card that fits your budget, credit situation, spending habits, and ability to pay on time.

For beginners, the best credit card is usually simple, affordable, easy to understand, and manageable.

Always read the official terms before applying.

Disclaimer

The information in this article is for educational purposes only and should not be considered financial, legal, tax, credit, banking, loan, or investment advice. Credit card fees, APRs, rewards, bonuses, benefits, approval requirements, payment terms, and issuer policies may change over time. Always review the official rates, fees, rewards terms, card agreement, and disclosures from the card issuer before applying for or using any credit card. If you have questions about your personal financial situation, consider speaking with a qualified professional.

Leave a Reply