Applying for a financial product can be an important decision.

A credit card, loan, bank account, finance app, or other financial product may affect your money, fees, credit, privacy, and daily financial habits.

For beginners, it can be difficult to know which product is a good fit.

Advertisements often highlight benefits, rewards, fast approval, low payments, or simple tools. But the full details may include fees, APR, requirements, limitations, and risks.

This is why reading reviews before applying can be helpful.

A good review can help you understand what a product offers, what it may cost, who it may fit, and what you should check before making a decision.

Why Reviews Matter for Beginners

Reviews matter because beginners may not always know what details to look for.

A financial product may look simple at first, but the real value depends on the full terms.

For example, a credit card may offer rewards, but it may also have a high APR or annual fee.

A loan may show a low monthly payment, but the total repayment cost may be higher than expected.

A bank account may advertise no monthly fee, but only if you meet certain requirements.

A finance app may offer useful tools, but it may charge a subscription or require account linking.

Reviews can help beginners notice these details before applying.

A good review may explain:

- Fees and costs

- APR and interest rates

- Requirements

- Features

- Benefits

- Risks

- Limitations

- Customer support

- Security and privacy

- Cancellation rules

- Who the product may fit

- Who should be careful

Reading reviews can help you make a more informed decision.

Reviews Help You Understand Costs

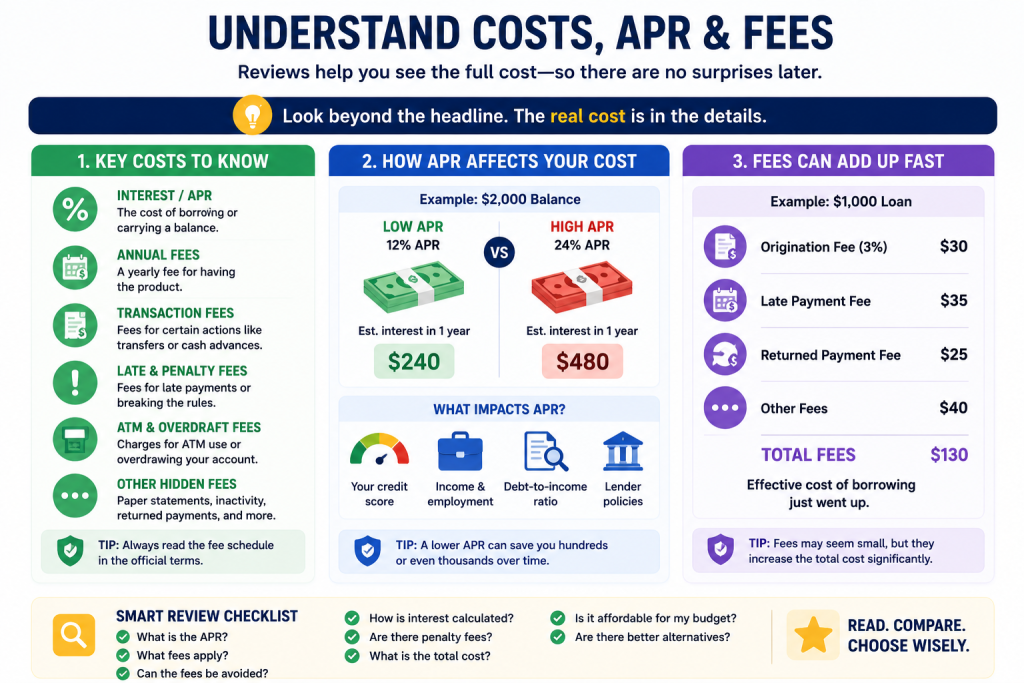

One of the most important reasons to read reviews is to understand costs.

Financial products can include many different fees.

For bank accounts, possible fees may include monthly maintenance fees, overdraft fees, ATM fees, transfer fees, wire fees, paper statement fees, and account closing fees.

For credit cards, possible fees may include annual fees, late payment fees, balance transfer fees, cash advance fees, foreign transaction fees, and penalty charges.

For loans, possible fees may include origination fees, application fees, late fees, returned payment fees, prepayment penalties, and service fees.

For finance apps, possible costs may include monthly subscriptions, annual subscriptions, premium plans, instant transfer fees, or paid features.

A review can help you see which fees are most important and when they may apply.

Before applying, ask:

- What fees can I be charged?

- Can these fees be avoided?

- Are the fees clearly explained?

- Are there lower-cost alternatives?

- Do the benefits justify the cost?

For beginners, products with clear and low fees are often easier to manage.

Reviews Explain APR and Fees

APR is another important detail that reviews can explain.

APR stands for Annual Percentage Rate.

APR is commonly used for credit cards and loans.

For credit cards, APR usually matters if you carry a balance from month to month. If you do not pay the full statement balance by the due date, interest may apply.

For loans, APR helps show the yearly cost of borrowing, including the interest rate and certain fees.

A review may explain:

- Purchase APR

- Balance transfer APR

- Cash advance APR

- Penalty APR

- Loan APR

- Introductory APR

- Regular APR after promotion

- Fixed or variable rate

- How APR affects total cost

APR can make borrowing expensive if you do not understand it.

A product with rewards or low monthly payments may still be costly if the APR is high.

Reviews can help beginners understand why APR matters before applying.

Reviews Show Product Features

Financial products often include many features.

Some features are useful, while others may not matter for your situation.

A credit card may offer cash back, points, travel benefits, purchase protection, fraud alerts, or credit score tools.

A bank account may offer mobile deposit, online bill pay, ATM access, account alerts, debit card controls, or savings tools.

A loan may offer fixed payments, flexible repayment terms, no prepayment penalty, or fast funding.

A finance app may offer budgeting tools, spending tracking, bill reminders, subscription monitoring, and savings goals.

A review can help explain which features are actually useful.

Before applying, ask:

- Do I need these features?

- Will I use them regularly?

- Are they free or paid?

- Are there limits?

- Do the features fit my habits?

- Are the benefits worth the cost?

A product with many features is not always better.

The best product is the one that fits your real needs.

Reviews Help You Compare Requirements

Many financial products have requirements.

Reviews can help you understand these before applying.

Credit cards may have credit score expectations, income review, identity verification, or approval standards.

Loans may require credit checks, income verification, employment information, debt review, collateral, or bank account information.

Bank accounts may require a minimum opening deposit, minimum balance, direct deposit, or monthly activity.

Finance apps may require account linking, identity verification, paid subscriptions, or personal data access.

Before applying, ask:

- Do I meet the basic requirements?

- Is approval likely?

- Will there be a hard credit check?

- Do I need to provide documents?

- Do I need to link an account?

- Can I meet any monthly requirements?

Understanding requirements can save time and help beginners avoid applying for products that may not fit their situation.

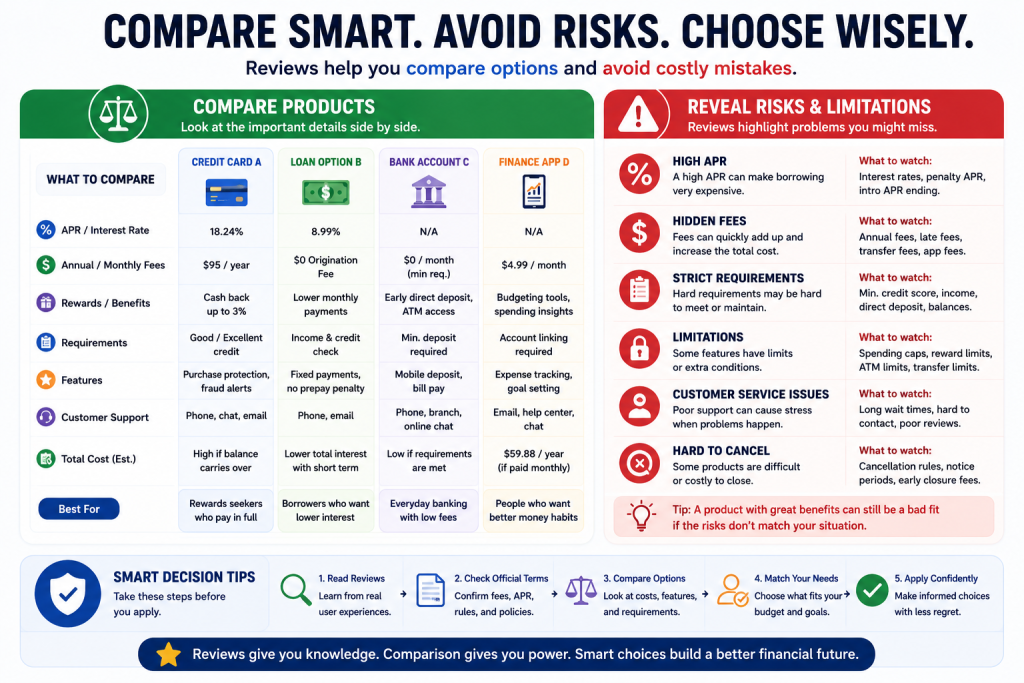

Reviews Can Reveal Risks and Limitations

A good review should explain both benefits and risks.

Financial products can have limitations that are easy to miss.

A credit card may have high APR, limited rewards, spending caps, rotating categories, or penalty fees.

A loan may have high total cost, origination fees, long repayment terms, late payment consequences, or prepayment penalties.

A bank account may have overdraft fees, ATM limits, minimum balance requirements, or transfer restrictions.

A finance app may have subscription fees, privacy concerns, account linking risks, limited free tools, or difficult cancellation.

Reviews can help beginners identify these risks before applying.

Ask:

- What could go wrong?

- What fees or penalties could apply?

- What happens if I miss a payment?

- What happens if I want to cancel?

- Are there limits or restrictions?

- Could this product create debt or stress?

A balanced review should not only describe what looks good.

It should also explain what to watch out for.

Reviews HelpYou Avoid Impulse Decisions

Financial products are often advertised in a way that encourages quick decisions.

You may see phrases like fast approval, limited-time bonus, instant access, easy cash, high rewards, or no fees.

These offers may sound attractive, but beginners should slow down before applying.

Reviews can help create distance between the advertisement and the decision.

Instead of applying immediately, read a review and compare the details.

Ask yourself:

- Do I really need this product?

- Does it solve a real problem?

- Can I afford any fees or payments?

- Do I understand the terms?

- Are there better options?

- Will this help or hurt my financial goals?

Taking time to review can help prevent unnecessary applications, unwanted fees, and poor financial decisions.

Always Check Official Terms Too

Reviews are useful, but they are not a replacement for official terms.

Financial product terms can change.

Fees, APRs, rewards, requirements, and policies may be updated by the provider.

A review may also summarize information and not include every detail.

Before applying, always check the official terms from the bank, lender, card issuer, app provider, or financial institution.

Review:

- Rates and fees

- APR

- Payment terms

- Account requirements

- Rewards rules

- Loan agreement

- Privacy policy

- Security information

- Cancellation rules

- Customer support

- Disclosures

The official terms are the final source for how the product works.

Use reviews to understand the product, then use official terms to confirm the details.

How to Read Reviews the Right Way

Not all reviews are equally helpful.

A useful review should be balanced, clear, and specific.

Look for reviews that explain:

- Who the product is best for

- Who should avoid it

- Fees and costs

- APR or interest rates

- Main features

- Requirements

- Pros and cons

- Risks and limitations

- Ease of use

- Customer support

- Security and privacy

- Fine print details

Be careful with reviews that only talk about benefits.

A review that never mentions fees, risks, or limitations may not give you the full picture.

Also compare more than one review when possible.

This can help you see different perspectives.

Compare Products Before Applying

Reading reviews is most useful when you compare multiple products.

Do not stop at the first option.

For credit cards, compare annual fees, APR, rewards, credit requirements, benefits, and penalties.

For loans, compare APR, fees, monthly payments, loan terms, total repayment cost, and lender requirements.

For bank accounts, compare monthly fees, minimum balance rules, ATM access, overdraft fees, and account features.

For finance apps, compare subscription costs, tools, security, privacy, account linking, and cancellation rules.

A simple comparison can help you choose a product that fits your needs better.

Common Beginner Mistakes

One common mistake is applying before reading reviews or terms.

Another mistake is choosing a product only because of advertising.

Some beginners focus only on rewards, bonuses, or fast approval.

Others ignore APR, fees, and payment rules.

Some people apply for loans without comparing total repayment cost.

Others sign up for finance apps without checking privacy or cancellation rules.

Another mistake is assuming a product is good for everyone because it has positive reviews.

A product can be good and still not fit your personal situation.

Reviews can help, but beginners still need to think about their own budget, habits, and goals.

Simple Checklist Before Applying

Before applying for a financial product, ask:

- Have I read at least one review?

- Have I checked the official terms?

- Do I understand the fees?

- Do I understand the APR or interest rate?

- Do I know the requirements?

- Do I understand the main features?

- Do I know the risks?

- Can I afford the cost?

- Does this product fit my habits?

- Can I cancel or close it easily?

- Have I compared alternatives?

- Does this product support my financial goals?

If you cannot answer these questions, take more time before applying.

Final Thoughts

Beginners should read reviews before applying because financial products can affect money, credit, fees, privacy, and long-term financial habits.

A good review can help explain costs, APR, fees, features, requirements, risks, limitations, support, and overall usefulness.

Reviews can also help you avoid impulse decisions and compare better options.

However, reviews should be used as a starting point.

Always check the official terms before applying.

For beginners, the best financial product is usually clear, affordable, useful, secure, and easy to understand.

Take your time, compare carefully, and choose the product that fits your real financial needs.

Disclaimer

The information in this article is for educational purposes only and should not be considered financial, legal, tax, credit, banking, loan, investment, cybersecurity, or privacy advice. Financial product reviews, fees, APRs, interest rates, rewards, requirements, account terms, loan terms, app policies, and provider information may change over time. Always review the official terms, disclosures, privacy policy, and fee schedule from the financial institution, lender, card issuer, app provider, or service provider before applying for or using any financial product. If you have questions about your personal financial situation, consider speaking with a qualified professional.

Leave a Reply