Choosing the right financial product can feel confusing, especially if you are just getting started with personal finance.

There are many options available, including checking accounts, savings accounts, credit cards, personal loans, budgeting apps, banking apps, and other financial tools.

Each product may have different fees, features, requirements, benefits, risks, and terms.

For beginners, the goal is not to choose the product that looks the most attractive in an advertisement. The goal is to choose a financial product that fits your real needs, budget, habits, and financial goals.

This guide explains how to choose the right financial product step by step.

Why Choosing the Right Financial Product Matters

Choosing the right financial product matters because financial products can affect your money, credit, fees, and daily financial life.

A good financial product can help you manage money more easily, save time, reduce fees, build credit, or organize your finances.

A poor choice can lead to unnecessary fees, high interest costs, confusing terms, missed payments, or financial stress.

For example, a checking account with high monthly fees may not be a good fit for someone who wants simple everyday banking.

A credit card with rewards may look attractive, but it may not be helpful if the annual fee is high or the APR is expensive.

A personal loan may seem useful, but it may become stressful if the monthly payment does not fit your budget.

This is why beginners should compare financial products carefully before signing up.

Know What Problem You Are Trying to Solve

Before choosing any financial product, ask yourself what problem you are trying to solve.

Different products are designed for different purposes.

A checking account may help with daily spending, bill payments, direct deposit, and debit card use.

A savings account may help store money for emergencies or future goals.

A credit card may help with convenience, credit building, rewards, or short-term purchases.

A personal loan may help with a larger one-time expense or debt consolidation.

A budgeting app may help track spending and organize money habits.

If you do not know why you need the product, it is easier to choose the wrong one.

Start with your goal first, then compare products that match that goal.

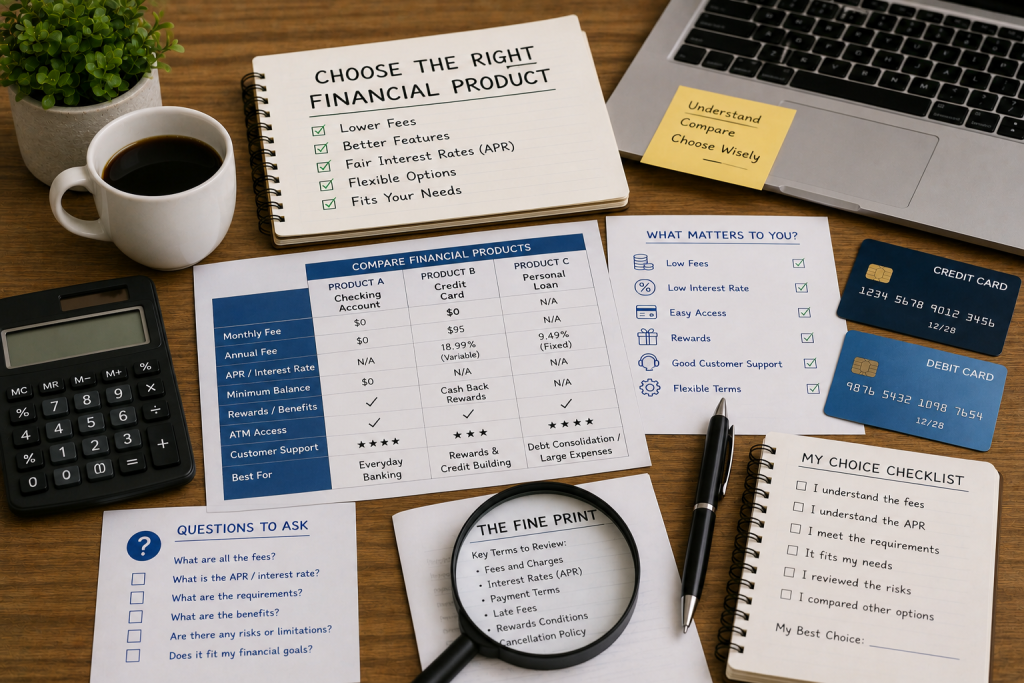

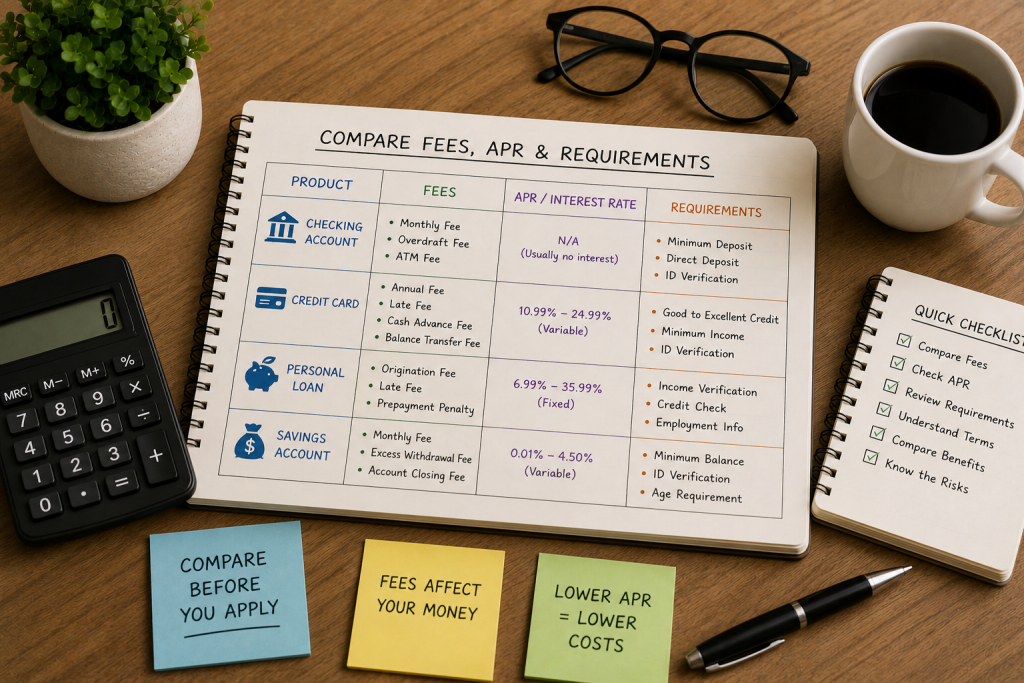

Compare Fees and Costs

Fees are one of the most important things to compare.

A financial product may look useful, but fees can make it more expensive than expected.

Common fees may include:

- Monthly maintenance fees

- Annual fees

- Late payment fees

- Overdraft fees

- ATM fees

- Origination fees

- Balance transfer fees

- Cash advance fees

- Foreign transaction fees

- Returned payment fees

- Subscription fees

- Account closing fees

Not every product has the same fees.

For example, a bank account may charge monthly maintenance fees or overdraft fees.

A credit card may charge annual fees, late fees, or cash advance fees.

A personal loan may charge origination fees, late fees, or prepayment penalties.

Before choosing a financial product, review the full fee schedule.

A product with fewer fees may be better for beginners who want something simple and easy to manage.

Understand APR and Interest Rates

APR and interest rates are especially important when comparing credit cards and loans.

APR stands for Annual Percentage Rate.

APR helps show the cost of borrowing money.

For credit cards, APR may apply if you carry a balance, take a cash advance, or use certain card features.

For personal loans, APR may include the interest rate and certain fees, giving a broader view of the cost of the loan.

Savings accounts may also have interest rates, but in that case the interest is money you may earn on your savings.

Before choosing a product, understand whether interest is something you pay or something you earn.

If you are borrowing money, a lower APR may reduce borrowing costs.

If you are saving money, a higher savings rate may help your money grow faster.

However, APR or interest rate should not be the only thing you compare. Fees, terms, requirements, and product features also matter.

Check Requirements Before Applying

Many financial products have requirements.

Before applying, check whether you are likely to qualify and whether the requirements fit your situation.

Bank accounts may have minimum deposit requirements, minimum balance rules, direct deposit requirements, or monthly activity requirements.

Credit cards may have credit score expectations, income requirements, identity verification, and approval standards.

Loans may require income verification, credit checks, employment information, debt review, collateral, or other documents.

Financial apps may require linking a bank account or sharing personal information.

Before applying, review the basic requirements carefully.

This can help you avoid applying for products that do not fit your situation.

Also pay attention to whether applying may involve a hard credit check. A hard inquiry may affect your credit score temporarily.

Compare Features and Benefits

Features and benefits can make a financial product more useful.

But not every feature matters to every person.

For a bank account, useful features may include:

- Mobile banking

- Online bill pay

- ATM access

- No monthly fee

- Direct deposit

- Account alerts

- Debit card controls

- Mobile check deposit

- Customer support

For a credit card, useful features may include:

- No annual fee

- Cash back rewards

- Fraud protection

- Purchase alerts

- Credit score tools

- Introductory APR offers

- Travel benefits

- Simple rewards structure

For a personal loan, useful features may include:

- Fixed monthly payments

- Clear repayment terms

- No prepayment penalty

- Fast funding

- Transparent fees

- Online account management

- Helpful customer support

Choose features that match your actual needs.

A product with many features is not always better if you will not use them.

Review Risks and Limitations

Every financial product may have risks or limitations.

A checking account may have overdraft fees or ATM fees.

A savings account may have withdrawal limits, low interest rates, or minimum balance requirements.

A credit card may have high APR, late fees, annual fees, or the risk of overspending.

A loan may create monthly payment pressure, interest costs, fees, and credit consequences if payments are missed.

A financial app may have subscription fees, data-sharing concerns, or limited customer support.

Before choosing a product, ask:

- What could go wrong?

- What fees could apply?

- What happens if I miss a payment?

- What happens if my balance is too low?

- What happens if I want to cancel?

- What are the limits?

- What information am I sharing?

Understanding the risks helps you avoid surprises later.

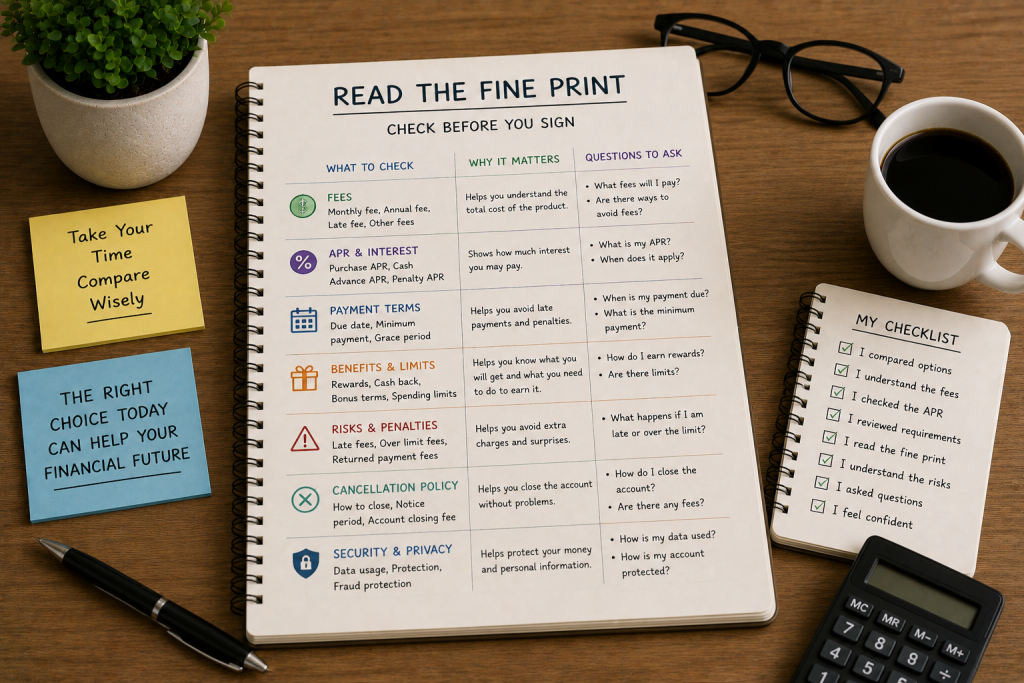

Read the Fine Print

The fine print is where many important details are found.

Advertisements often highlight benefits, but the official terms explain the real rules.

Before signing up, read the product terms carefully.

Check:

- Fees

- APR

- Interest rates

- Minimum balance rules

- Payment due dates

- Late payment rules

- Rewards limits

- Loan repayment terms

- Account requirements

- Withdrawal rules

- Cancellation terms

- Promotional offer expiration dates

- Security policies

- Customer support options

If something is unclear, ask the company before applying.

Do not sign up for a financial product only because the main offer looks good.

The details matter.

Avoid Choosing Only Based on Advertising

Financial product advertising is designed to attract attention.

An advertisement may highlight cash bonuses, rewards, fast approval, no fees, low payments, or special features.

These benefits may be real, but they may also come with conditions.

For example, a bank account bonus may require direct deposit or a minimum balance.

A credit card rewards offer may require spending a certain amount.

A loan with a low monthly payment may have a long repayment term and higher total cost.

A financial app may offer a free trial but charge a subscription later.

Before choosing based on advertising, read the full terms and compare alternatives.

A good financial product should still make sense after you review the details.

Compare More Than One Option

It is usually smart to compare more than one option.

If you only look at one product, you may not know whether the fees, APR, features, or requirements are reasonable.

Try comparing at least three options when possible.

When comparing, look at:

- Fees

- APR or interest rate

- Monthly cost

- Features

- Requirements

- Customer support

- Security

- Reviews

- Ease of use

- Limitations

- Cancellation rules

Use the same comparison points for each product.

This makes it easier to see which one fits your needs best.

Think About Your Habits

Your personal habits matter when choosing a financial product.

A product that works well for one person may not work well for another.

If you often forget due dates, a credit card with high late fees may be risky unless you set reminders or automatic payments.

If you prefer in-person banking, an online-only bank may not be the best fit.

If you often use cash, choose a bank account with good ATM access.

If you are trying to avoid debt, be careful with credit cards and loans.

If you want simple money management, choose products with clear terms and low fees.

The right financial product should fit your real behavior, not an ideal version of yourself.

Check Customer Support

Customer support is important because financial products can involve problems or questions.

You may need help with account access, payments, fraud alerts, transaction issues, card replacement, loan payoff, app problems, or billing questions.

Before choosing a product, check how customer support works.

Look for:

- Phone support

- Live chat

- Secure messaging

- Email support

- Help center articles

- Branch access

- Support hours

- Fraud support

- Response times

A product may look good, but poor support can become frustrating if something goes wrong.

Good customer support can be especially important for beginners.

Consider Security and Privacy

Security is important when choosing financial products, especially apps and online accounts.

Before signing up, check whether the company provides basic security features.

Useful security features may include:

- Two-factor authentication

- Account alerts

- Fraud monitoring

- Secure login

- Debit or credit card lock

- Password protection

- Encrypted connections

- Official mobile apps

- Clear privacy policy

Also consider what information the company collects and how it may be used.

Be careful with financial apps or websites that are unclear about security, privacy, fees, or ownership.

Use official websites and app stores when applying or downloading apps.

Common Beginner Mistakes

One common mistake is choosing a product only because it offers a bonus or reward.

A bonus may not be worth it if the product has high fees or does not fit your needs.

Another mistake is ignoring APR.

For credit cards and loans, APR can make borrowing expensive if you carry a balance or repay over time.

Some beginners ignore monthly fees, annual fees, overdraft fees, or origination fees.

Another mistake is applying before checking requirements.

Some people also choose products that are too complicated.

Simple products are often better for beginners.

It is also a mistake to skip the fine print.

The details can change the real value of the product.

How to Make a Final Decision

Before choosing a financial product, review everything together.

Ask yourself:

- What do I need this product for?

- Does it solve a real problem?

- What fees apply?

- What is the APR or interest rate?

- Can I meet the requirements?

- Do the features match my needs?

- What are the risks?

- Can I understand the terms?

- Is customer support easy to reach?

- Are there better alternatives?

If the product is simple, affordable, useful, and easy to understand, it may be a better fit.

If the product feels confusing, expensive, or risky, keep comparing.

Final Thoughts

Choosing the right financial product is an important part of managing money.

Whether you are opening a bank account, applying for a credit card, comparing a loan, or choosing a financial app, the process should start with your real needs.

Know what problem you are trying to solve.

Compare fees, APR, requirements, features, risks, support, security, and fine print.

Avoid choosing only because of advertising, bonuses, or fast approval.

For beginners, the best financial product is usually simple, clear, affordable, and useful for your actual financial life.

Disclaimer

The information in this article is for educational purposes only and should not be considered financial, legal, tax, credit, loan, or investment advice. Financial products, fees, APRs, interest rates, rewards, approval requirements, account terms, and provider policies may change over time. Always review the official terms and disclosures from the financial institution, lender, card issuer, or service provider before applying for or using any financial product. If you have questions about your personal financial situation, consider speaking with a qualified professional.

Leave a Reply