If you are new to credit cards, you may see two common terms: secured credit card and unsecured credit card. These two types of cards can look similar, but they work differently.

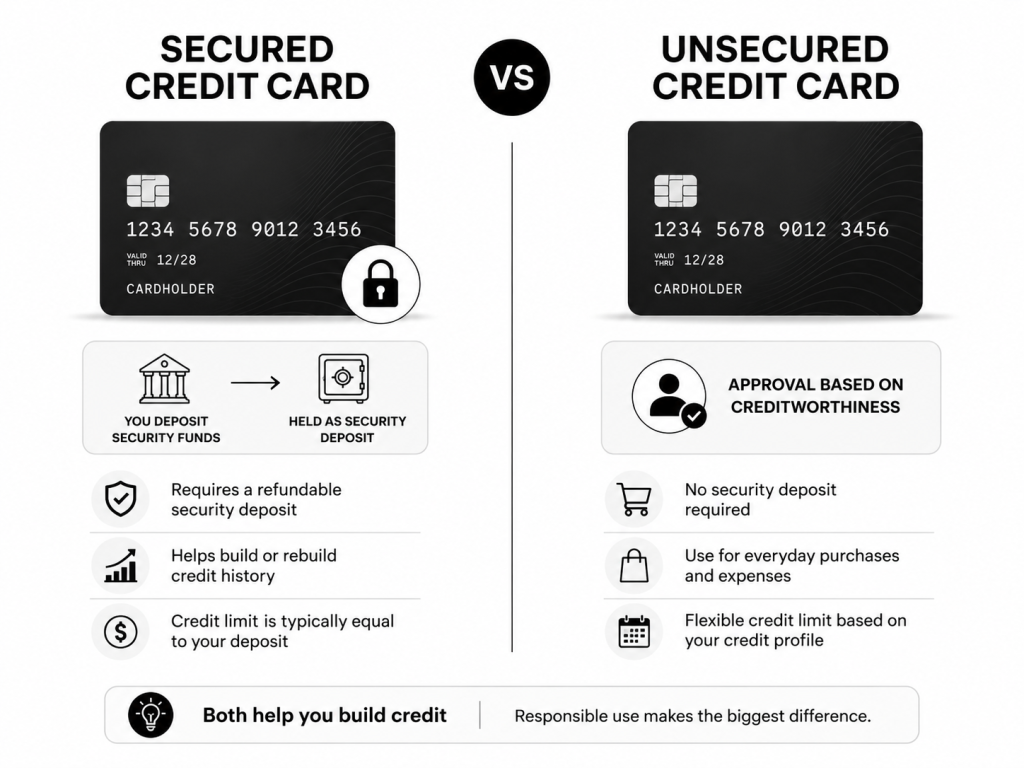

The biggest difference is simple: a secured credit card usually requires a refundable security deposit, while an unsecured credit card does not.

Both types of cards can help you build credit when used responsibly. But the right choice depends on your credit history, financial situation, and approval options.

This guide explains how secured and unsecured credit cards work, the main differences between them, and how beginners can choose the right option.

What Is a Secured Credit Card?

A secured credit card is a credit card that usually requires a refundable security deposit.

The deposit helps reduce risk for the card issuer. If you do not pay your balance, the issuer may use your deposit to cover what you owe, depending on the card’s terms.

For example, if you deposit $300, your credit limit may be $300. If you deposit $500, your credit limit may be $500.

This does not mean you are spending your own deposit every time you use the card. You still make purchases with the credit card and receive a bill. You are expected to pay the bill just like any other credit card.

The deposit is usually held as security while the account is open. If you close the account in good standing or upgrade to an unsecured card, the deposit may be returned according to the issuer’s rules.

Secured cards are often used by people who are new to credit, rebuilding credit, or having trouble getting approved for regular credit cards.

What Is an Unsecured Credit Card?

An unsecured credit card is a regular credit card that does not require a security deposit.

Approval is usually based on your credit profile, income, debt, payment history, and other factors reviewed by the card issuer.

Most standard credit cards are unsecured cards. They may include beginner cards, cash back cards, travel cards, balance transfer cards, and premium cards.

With an unsecured card, the issuer gives you a credit limit based on your creditworthiness. You can use the card for purchases, then repay the balance according to the billing cycle.

If you manage the card responsibly, an unsecured card can help you build credit, earn rewards, and access higher credit limits over time.

However, if you miss payments or carry high balances, it can hurt your credit and lead to fees or interest charges.

The Main Difference Between Secured and Unsecured Cards

The main difference is the security deposit.

A secured credit card usually requires a refundable deposit before you can use the card. An unsecured credit card does not require that deposit.

Another difference is approval difficulty. Secured cards are often easier to qualify for because the deposit reduces the issuer’s risk. Unsecured cards may require a stronger credit profile.

Credit limits may also differ. With a secured card, your credit limit is often connected to your deposit amount. With an unsecured card, the credit limit is usually based on your financial and credit profile.

Both cards can report your payment history to credit bureaus, but you should always check the issuer’s terms. If your goal is building credit, reporting to major credit bureaus is very important.

Who Should Consider a Secured Credit Card?

A secured credit card may be a good option if you are new to credit or have a limited credit history.

It may also help if your credit score is low or if you have been denied for unsecured credit cards.

Secured cards can be useful for:

- First-time credit card users

- Students building credit

- People with no credit history

- People rebuilding credit

- People who want a controlled starting point

People who have trouble getting approved for unsecured cards

A secured card can act as a bridge. You start with a deposit-backed card, build responsible habits, and may later qualify for an unsecured card.

The goal is not to stay with a secured card forever. The goal is to use it carefully and build a stronger credit profile over time.

Who Should Consider an Unsecured Credit Card?

An unsecured credit card may be better if you already have some credit history and can qualify for approval.

It may also be a better option if you do not want to provide a security deposit.

Unsecured cards may offer better rewards, higher credit limits, sign-up bonuses, or additional benefits. But they may also come with higher risks if used carelessly.

An unsecured card may be a good fit if:

- You have a fair or good credit profile

- You can get approved without a deposit

- You want rewards such as cash back

- You can pay your balance on time

- You understand interest, fees, and credit utilization

- You can manage credit responsibly

For beginners with no credit history, approval may be harder. In that case, a secured card may be a better first step.

Pros of Secured Credit Cards

Secured credit cards can be helpful for beginners because they are often easier to qualify for.

They can help you build or rebuild credit if the issuer reports to the major credit bureaus.

They may also encourage responsible habits because the credit limit is usually lower and connected to your deposit.

Some secured cards can later be upgraded to unsecured cards. If that happens, your deposit may be returned and your account may continue with better terms.

Secured cards are also useful because they teach the basics of credit card management: making payments, tracking balances, and keeping utilization low.

Cons of Secured Credit Cards

The biggest downside is the security deposit.

You need to provide money upfront before using the card. This can be difficult if your budget is tight.

Another downside is that secured cards may have fewer rewards or benefits compared with unsecured cards.

Some secured cards may also charge fees, so you need to read the terms carefully. A secured card is not automatically a good card just because it is easier to get.

You should check:

- Annual fee

- APR

- Late payment fee

- Deposit requirements

- Credit bureau reporting

- Upgrade options

- Refund rules for the deposit

A good secured card should help you build credit without adding unnecessary costs.

Pros of Unsecured Credit Cards

Unsecured credit cards do not require a security deposit, which makes them more convenient for many users.

They may offer cash back, points, travel rewards, purchase protection, or other benefits depending on the card.

They may also offer higher credit limits over time if you manage the account responsibly.

For people with established credit, unsecured cards can provide more flexibility and more reward options.

Unsecured cards are also easier to keep long term because you do not have money tied up in a deposit.

Cons of Unsecured Credit Cards

Unsecured cards can be harder to qualify for if you have no credit history or poor credit.

Some unsecured cards may have high APRs, annual fees, or penalty fees.

Because there is no deposit limit controlling your starting risk, it can also be easier to overspend if you are not careful.

Beginners should remember that a credit limit is not extra income. It is borrowed money that must be repaid.

If you miss payments, carry high balances, or apply for too many cards, your credit profile may be affected.

Can a Secured Card Help Build Credit?

Yes, a secured card can help build credit if it is used responsibly and reported to the major credit bureaus.

The most important habits are:

- Pay on time every month

- Keep your balance low

- Avoid maxing out the card

- Pay the full balance when possible

- Use the card regularly but carefully

- Do not apply for too many cards at once

Payment history is one of the most important parts of a credit profile. Paying on time can help show lenders that you are responsible.

Credit utilization also matters. If your card has a $300 limit, try not to keep a high balance on it. Many beginners aim to keep utilization below 30%, and lower can be better.

When Can You Upgrade From Secured to Unsecured?

Some issuers may review your account after several months of responsible use.

If you make on-time payments and keep your account in good standing, the issuer may allow you to upgrade to an unsecured card.

When that happens, your security deposit may be refunded according to the issuer’s rules.

However, not every secured card has an upgrade path. Before applying, check whether the issuer offers account reviews or graduation to an unsecured card.

If the card does not offer an upgrade path, you may still be able to build credit and later apply for an unsecured card separately.

How to Choose Between Secured and Unsecured Cards

If you can qualify for a simple, low-cost unsecured credit card, that may be a good choice.

But if you are new to credit or cannot get approved, a secured card may be a better starting point.

Ask yourself these questions:

- Do I have credit history?

- Have I been denied for unsecured cards?

- Can I afford a refundable deposit?

- Does the card report to major credit bureaus?

- Are the fees reasonable?

- Can I pay the balance on time every month?

- Does the card offer a path to upgrade?

The best card is not always the one with the most rewards. For beginners, the best card is often the one that is simple, affordable, and easy to manage.

How to Use Either Card Responsibly

Whether you choose a secured or unsecured card, responsible use is what matters most.

Use the card only for purchases you can afford. Pay the bill on time every month. Keep your balance low. Avoid using the card for cash advances. Review your statement regularly.

If possible, pay your full statement balance by the due date. This can help you avoid interest on purchases.

Also avoid applying for multiple cards at once. Starting with one card and managing it well is often better than opening several accounts too quickly.

Good credit is built through consistent habits over time.

Final Thoughts

Secured and unsecured credit cards can both be useful tools for building credit.

A secured credit card usually requires a refundable security deposit and may be easier to qualify for. It can be a smart starting point for beginners, students, or people rebuilding credit.

An unsecured credit card does not require a deposit and may offer more rewards or flexibility, but it can be harder to qualify for if your credit history is limited.

The right choice depends on your situation. If you are just starting out, a secured card can help you build a foundation. If you already qualify for an unsecured card, a simple beginner-friendly unsecured card may be enough.

No matter which type you choose, the key is responsible use. Pay on time, keep balances low, and avoid spending more than you can afford to repay.

Disclaimer

The information in this article is for educational purposes only and should not be considered financial, legal, tax, credit, or investment advice. Credit card terms, fees, deposit requirements, APRs, rewards, approval requirements, and reporting policies may change over time. Always review the official terms and disclosures from the card issuer before applying or using any credit card. If you have questions about your personal financial situation, consider speaking with a qualified professional.

Leave a Reply