Cash back credit cards are one of the easiest types of credit card rewards to understand. Instead of earning complicated points or travel miles, you earn a small percentage of your spending back as cash back rewards.

For beginners, this can be simple and useful. You use your card for normal purchases, pay your bill responsibly, and earn a small amount back over time.

However, cash back is not free money if you overspend or carry a balance. Interest charges and fees can easily be higher than the rewards you earn.

This guide explains how cash back credit cards work, the different types of cash back rewards, what to compare before applying, and how to use these cards wisely.

What Is a Cash Back Credit Card?

A cash back credit card is a credit card that gives you back a percentage of eligible purchases.

For example, if a card offers 1.5% cash back and you spend $100 on eligible purchases, you may earn $1.50 in cash back.

The exact amount depends on the card’s reward rate and the type of purchase. Some cards offer the same cash back rate on every purchase. Others offer higher rewards in certain categories, such as groceries, gas, dining, or online shopping.

Cash back rewards are popular because they are easy to understand. You spend money on normal purchases, and a small portion comes back to you as a reward.

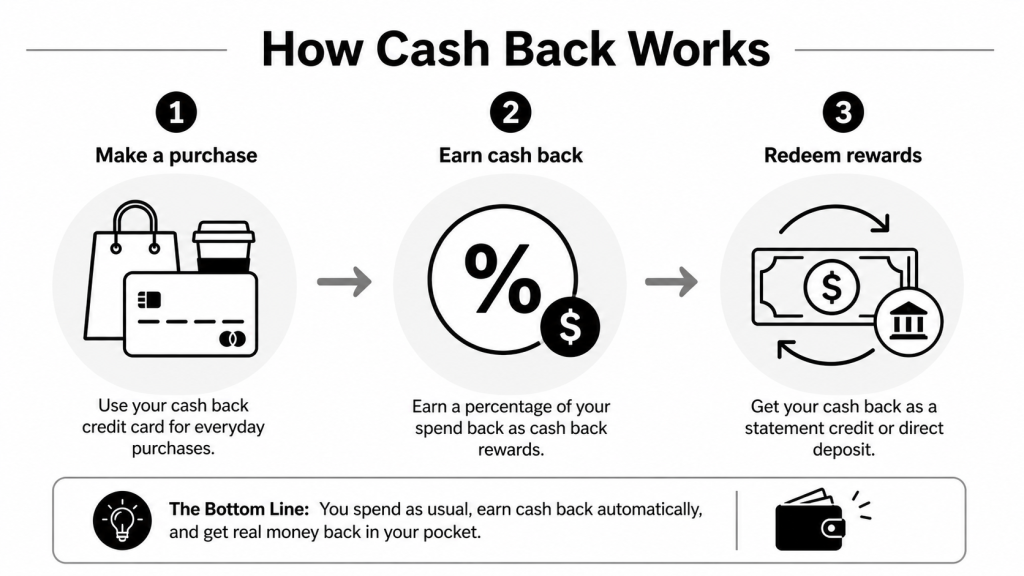

How Cash Back Rewards Work

Cash back rewards usually work in a simple way.

First, you make an eligible purchase using your credit card.

Second, the card issuer calculates the cash back reward based on the card’s reward rate.

Third, the reward is added to your account after the purchase is processed.

For example, if your card earns 2% cash back on groceries and you spend $200 on groceries, you may earn $4 in cash back.

That may not sound like a lot, but over time, rewards can add up if you use the card responsibly.

The key is to remember that cash back rewards only help you if you avoid unnecessary interest and fees.

Common Types of Cash Back Credit Cards

There are several types of cash back credit cards. Beginners should understand the differences before applying.

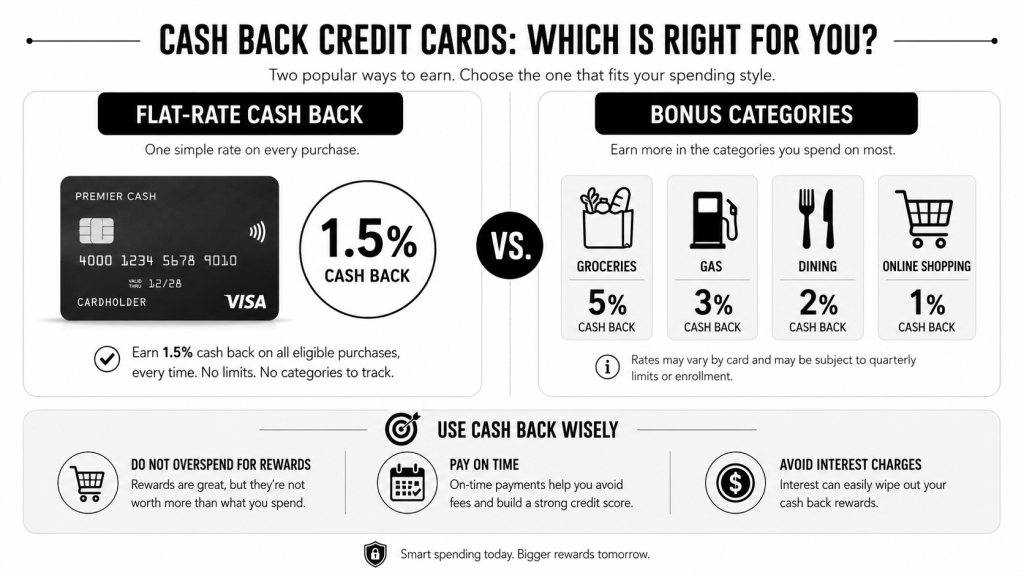

Flat-Rate Cash Back Cards

A flat-rate cash back card gives the same reward rate on most purchases.

For example, a card may offer 1.5% cash back on all eligible purchases.

This type of card is simple and beginner-friendly because you do not need to track categories or remember special rules.

If you want an easy card for everyday use, a flat-rate cash back card may be a good starting point.

Bonus Category Cash Back Cards

Some cards offer higher cash back rates in specific categories.

For example, a card may offer:

- 3% cash back on groceries

- 2% cash back on gas

- 1% cash back on all other purchases

These cards can be useful if the bonus categories match your normal spending. However, they require more attention because not every purchase earns the same rate.

Rotating Category Cash Back Cards

Some cash back cards offer higher rewards in categories that change every few months.

For example, one quarter may focus on groceries, while another quarter may focus on gas or online shopping.

These cards can offer strong rewards, but they may not be ideal for beginners because they often require activation, tracking, and planning.

If you forget to activate the category or spend outside the bonus categories, you may earn less than expected.

How You Can Redeem Cash Back

Cash back rewards can usually be redeemed in different ways, depending on the card issuer.

Common redemption options include:

- Statement credit

- Direct deposit

- Check

- Gift cards

- Travel credit

- Online shopping credit

A statement credit reduces your credit card balance. For example, if you have $25 in rewards, you may apply it as a credit to your account.

A direct deposit sends the money to your bank account if the issuer supports that option.

Some cards may also allow you to redeem rewards for gift cards or travel, but the value may vary.

Before applying, check how the card allows you to redeem rewards and whether there is a minimum redemption amount.

Why Cash Back Cards Are Popular With Beginners

Cash back cards are popular with beginners because the rewards are easy to understand.

Points and miles can be useful, but they often require more knowledge. You may need to understand airline partners, hotel programs, transfer values, redemption charts, or travel rules.

Cash back is simpler.

If you earn $10 in cash back, the value is usually easier to understand than 10,000 points.

For a beginner, simplicity matters. A simple reward system can help you focus on responsible credit habits instead of chasing complicated benefits.

What to Compare Before Applying

Before applying for a cash back credit card, compare more than just the reward rate.

First, check whether the card has an annual fee. Some cash back cards have no annual fee, while others may charge one. If a card charges a fee, make sure the rewards and benefits are worth the cost.

Second, check the APR. If you carry a balance, interest charges can quickly wipe out your cash back rewards.

Third, review the reward categories. A card is only useful if the categories match your real spending habits.

Fourth, check whether there are limits on rewards. Some cards only offer higher cash back up to a certain spending amount.

Fifth, review the redemption rules. Some cards may require a minimum amount before you can redeem rewards.

Finally, check foreign transaction fees if you travel internationally or shop from foreign websites.

Cash Back vs Interest Charges

This is one of the most important things beginners should understand.

Cash back rewards are usually small compared to credit card interest.

For example, earning 1% or 2% cash back is helpful, but if you carry a balance and pay high interest, you may lose much more than you earn.

This is why cash back cards are best for people who pay their balance in full each month.

If you carry a balance, the main goal should be paying down debt, not earning rewards.

Rewards should never be a reason to spend more than you can afford.

Common Mistakes to Avoid

One common mistake is overspending just to earn rewards.

If you buy something you do not need just to earn cash back, you are not saving money. You are spending more money.

Another mistake is ignoring APR. A card with good rewards can still be expensive if you carry a balance.

Some users also forget that bonus categories may have limits, restrictions, or activation requirements.

Another mistake is choosing a card based on the highest advertised reward rate without checking whether that rate applies to your normal spending.

Beginners should focus on simple value, not marketing hype.

How to Use a Cash Back Card Wisely

A cash back card can be useful if you use it with discipline.

Start by using the card only for purchases you already planned to make. This may include groceries, gas, phone bills, or small monthly subscriptions.

Track your spending during the month so you do not accidentally spend more than your budget allows.

Pay your full statement balance by the due date whenever possible. This helps you avoid interest and keeps the rewards valuable.

Keep your credit utilization low. Using too much of your credit limit may affect your credit score, even if you pay on time.

Also review your rewards occasionally. Make sure you understand how much you are earning and whether the card still fits your spending habits.

Should Beginners Get a Cash Back Credit Card?

A cash back credit card can be a good choice for beginners if it is simple, low-cost, and easy to manage.

For many beginners, a no annual fee cash back card with a simple flat-rate reward may be a practical starting point.

However, cash back should not be the only reason to choose a card.

You should also consider the APR, fees, approval requirements, credit limit, reporting to credit bureaus, and how easy the card is to manage.

If you are still building credit, you may need to start with a secured card or a beginner-friendly card first.

Final Thoughts

Cash back credit cards can be a simple way to earn rewards on everyday purchases. They are easy to understand, beginner-friendly, and often more straightforward than travel points or miles.

But cash back rewards only make sense when you use the card responsibly.

If you pay interest, miss payments, or overspend, the rewards may not be worth it.

For beginners, the best strategy is simple: choose a card you understand, use it for normal purchases, pay the balance on time, and avoid spending more just to earn rewards.

Cash back can be useful, but good credit habits are more important.

Disclaimer

The information in this article is for educational purposes only and should not be considered financial, legal, tax, credit, or investment advice. Credit card rewards, fees, APRs, terms, redemption options, and approval requirements may change over time. Always review the official terms and disclosures from the credit card issuer before applying or using any credit card. If you have questions about your personal financial situation, consider speaking with a qualified professional.

Leave a Reply