Personal loans and credit cards are two common ways to borrow money. Both can be useful in certain situations, but they work very differently.

A personal loan usually gives you a fixed amount of money upfront and a set repayment schedule. A credit card gives you a revolving credit limit that you can use, repay, and use again.

For beginners, it is important to understand the difference before borrowing. Choosing the wrong option can lead to higher costs, difficult payments, or long-term debt.

This guide explains how personal loans and credit cards compare, including repayment structure, APR, fees, monthly payments, and when each option may make sense.

Why This Comparison Matters

Borrowing money is a financial decision that can affect your budget, credit, and future financial flexibility.

Some people use personal loans for larger one-time expenses. Others use credit cards for smaller purchases, emergencies, or short-term spending.

The right choice depends on the purpose of the borrowing, the cost, the repayment plan, and your ability to manage payments.

A personal loan may feel more structured because the payments are usually fixed.

A credit card may feel more flexible because you can use it again after paying down the balance.

However, flexibility can also create risk if spending is not controlled.

Before choosing either option, compare the full cost and repayment responsibility.

What Is a Personal Loan?

A personal loan is money borrowed from a bank, credit union, or online lender.

In most cases, the lender gives you a lump sum of money, and you repay it over time through scheduled payments.

Personal loans are often installment loans. This means you make regular payments, usually monthly, until the loan is fully paid off.

A personal loan may have a fixed interest rate, fixed monthly payment, and fixed repayment term.

For example, if you borrow $10,000 for three years, you may make the same monthly payment every month until the loan is paid off.

Personal loans may be used for debt consolidation, home repairs, medical expenses, moving costs, large purchases, or other personal needs.

What Is a Credit Card?

A credit card is a revolving line of credit.

Instead of receiving one lump sum, you get a credit limit. You can spend up to that limit, repay some or all of the balance, and use the available credit again.

For example, if your credit card limit is $3,000 and you spend $500, you may have $2,500 available. If you repay the $500, your available credit may return to $3,000.

Credit cards are often used for daily purchases, online shopping, travel, subscriptions, emergencies, and rewards.

If you pay your full statement balance by the due date, you may avoid interest on purchases, depending on the card terms.

If you carry a balance, interest can become expensive.

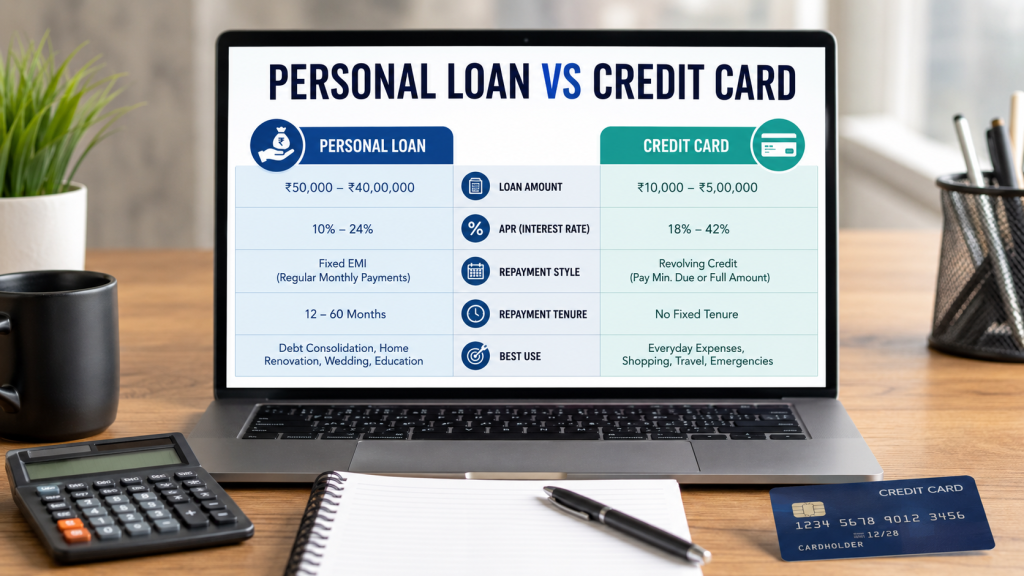

Main Difference Between Personal Loans and Credit Cards

The main difference is repayment structure.

A personal loan usually has a fixed loan amount, fixed repayment term, and fixed monthly payment.

A credit card has a revolving credit limit, flexible spending, and a minimum monthly payment.

With a personal loan, you borrow once and repay over time.

With a credit card, you can borrow repeatedly as long as you have available credit.

This makes personal loans more structured and credit cards more flexible.

For beginners, structure can be helpful if you want a clear payoff plan. Flexibility can be useful, but it can also make it easier to overspend.

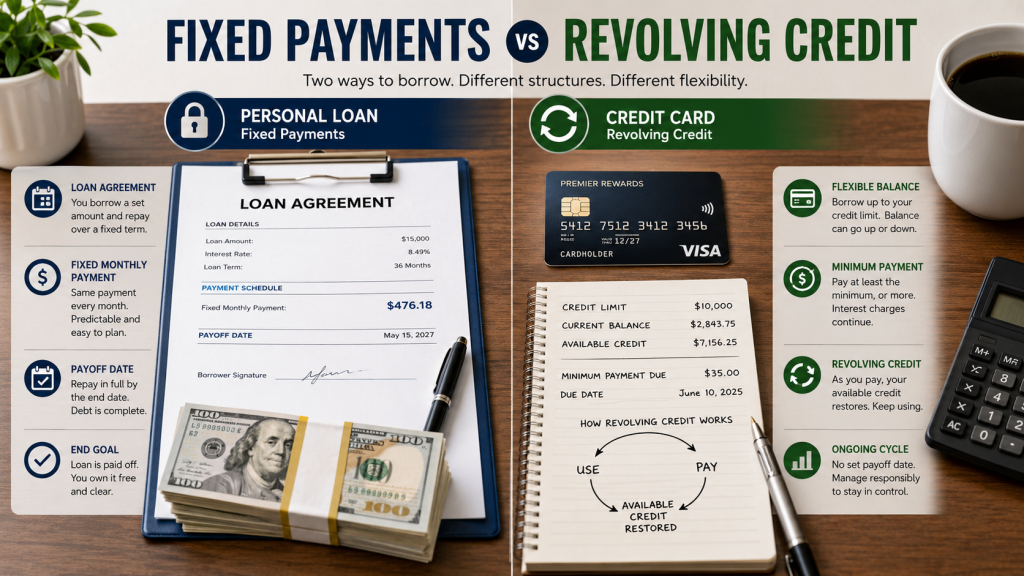

Fixed Payments vs Revolving Credit

Personal loans usually have fixed payments.

This means you know how much you need to pay every month and when the loan should be paid off.

This can make budgeting easier.

Credit cards are different. They allow revolving credit.

You may only be required to make a minimum payment each month. However, paying only the minimum can keep you in debt longer and increase total interest.

A credit card balance can continue if you keep spending while only making small payments.

This is one reason credit cards can become difficult to manage.

If you want a clear repayment schedule, a personal loan may be easier to understand.

If you need short-term flexibility and can pay the full balance, a credit card may be useful.

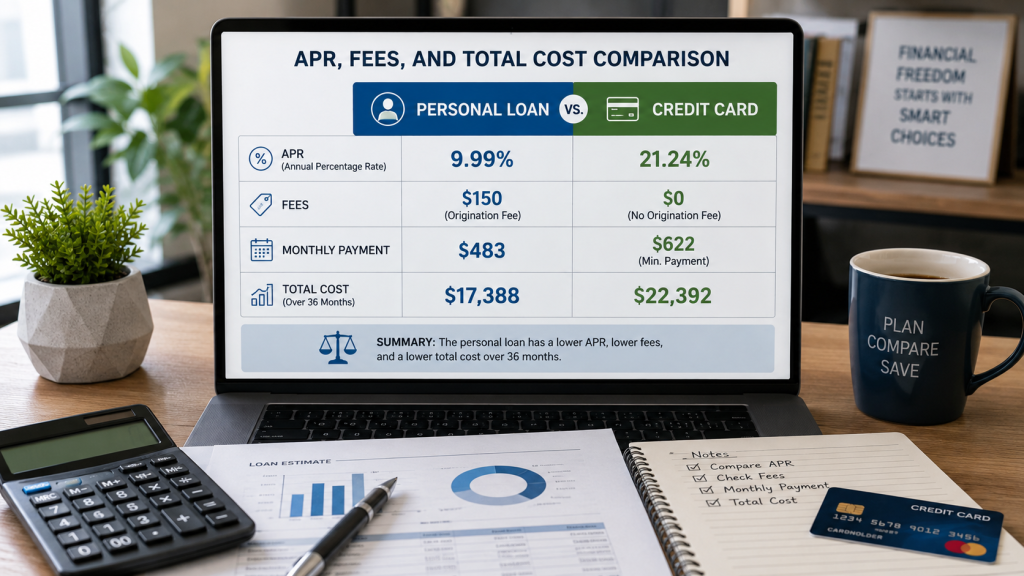

APR and Interest Costs

APR stands for Annual Percentage Rate.

APR helps show the cost of borrowing money.

Both personal loans and credit cards can have APRs, but they may work differently.

A personal loan APR may include the interest rate and certain loan fees. The APR helps you understand the cost of the loan over time.

A credit card APR applies when you carry a balance, take a cash advance, or use certain card features that create interest.

Credit card APRs can often be higher than personal loan APRs, depending on the borrower, lender, card issuer, and market conditions.

However, a credit card may not charge interest on purchases if you pay the full statement balance on time.

This is why repayment behavior matters.

A credit card can be expensive if you carry a balance. But it can be low-cost for purchases if paid in full each month.

Fees to Compare

Both personal loans and credit cards can have fees.

Personal loan fees may include:

- Origination fees

- Late payment fees

- Returned payment fees

- Prepayment penalties

- Application fees

- Processing fees

Credit card fees may include:

- Annual fees

- Late payment fees

- Balance transfer fees

- Cash advance fees

- Foreign transaction fees

- Returned payment fees

- Over-limit fees

Not every loan or credit card has the same fees.

Before choosing either option, review the terms carefully.

A personal loan with a low interest rate but a high origination fee may cost more than expected.

A credit card with rewards may look attractive but could have a high APR or annual fee.

Always compare the full cost, not just one number.

When a Personal Loan May Make Sense

A personal loan may make sense when you need a larger amount of money for a planned purpose and want a fixed repayment schedule.

It may be useful for:

- Debt consolidation

- Home repairs

- Medical expenses

- Moving costs

- Large necessary purchases

- Emergency expenses

- Predictable repayment planning

A personal loan may also make sense if the APR is lower than your credit card APR and you are using it to consolidate debt.

However, debt consolidation only helps if you avoid creating new debt afterward.

A personal loan can give structure, but it still creates monthly payment responsibility.

Before applying, make sure the payment fits your budget.

When a Credit Card May Make Sense

A credit card may make sense for smaller purchases, short-term expenses, online payments, travel, or emergency flexibility.

It may also be useful if you can pay the full statement balance every month.

Credit cards may offer benefits such as rewards, purchase protection, fraud protection, travel benefits, or convenience.

However, credit cards can become expensive if you carry a balance.

If you only make minimum payments, interest can add up quickly.

A credit card may be useful when you need flexibility and have the discipline to repay quickly.

It may not be a good choice for long-term borrowing if the APR is high.

Debt Consolidation: Loan or Credit Card?

Debt consolidation means combining multiple debts into one payment or lower-cost option.

A personal loan may be used to pay off multiple credit card balances. Then you repay the loan with a fixed monthly payment.

This can be helpful if the loan has a lower APR than the credit cards and the borrower stops adding new credit card debt.

A balance transfer credit card may also be used for debt consolidation. Some cards offer a promotional APR for a limited time.

However, balance transfer cards may have fees and the promotional rate may end after a certain period.

If the balance is not paid off before the promotional period ends, interest costs may increase.

When comparing debt consolidation options, review APR, fees, repayment period, total cost, and your ability to avoid new debt.

Which Option Is Better for Emergencies?

For emergencies, the better option depends on the situation.

A credit card may be faster if you need to pay immediately and already have available credit.

A personal loan may be better for a larger emergency expense if you need a structured repayment plan and can qualify for reasonable terms.

However, borrowing for emergencies can be risky if the repayment plan is unclear.

This is why building an emergency fund is important.

Savings can reduce the need to rely on credit cards or personal loans when unexpected costs happen.

How Credit Score Can Be Affected

Both personal loans and credit cards can affect your credit.

A personal loan may affect your credit through the application, payment history, loan balance, and account age.

On-time payments may help build positive credit history.

Late or missed payments can damage your credit.

A credit card can also affect your credit through payment history, credit utilization, account age, and credit inquiries.

Credit utilization means how much of your available credit you are using.

Using a high percentage of your credit limit can affect your credit score.

Whether you choose a personal loan or credit card, making payments on time is very important.

Common Beginner Mistakes to Avoid

One common mistake is using a credit card like extra income.

A credit card is borrowed money, not free money.

Another mistake is taking a personal loan without understanding the total repayment cost.

Some beginners choose based only on the monthly payment and ignore APR, fees, or loan term.

Another mistake is using a personal loan to pay off credit cards and then continuing to build new credit card balances.

This can create more debt than before.

Some people also ignore late payment fees, cash advance fees, balance transfer fees, and origination fees.

Before borrowing, understand the full cost and have a repayment plan.

How to Decide Which Is Better

To decide between a personal loan and a credit card, ask yourself several questions.

- How much money do I need to borrow?

- Is this a one-time expense or ongoing spending?

- Can I repay the balance quickly?

- Do I need a fixed monthly payment?

- What is the APR?

- What fees apply?

- How long will repayment take?

- Will this payment fit my budget?

- Am I likely to keep spending after borrowing?

If you need structure and a clear payoff date, a personal loan may be better.

If you need short-term flexibility and can pay in full, a credit card may be better.

The best choice is the one that fits your situation and costs the least while remaining manageable.

Final Thoughts

Personal loans and credit cards can both be useful financial tools, but they serve different purposes.

A personal loan provides a fixed amount of money with a set repayment schedule.

A credit card provides revolving credit that can be used repeatedly.

A personal loan may be better for larger planned expenses, debt consolidation, or borrowers who want predictable payments.

A credit card may be better for smaller purchases, convenience, rewards, or short-term spending that can be paid off quickly.

Before choosing either option, compare APR, fees, repayment structure, total cost, and your ability to make payments on time.

The safest choice is the one you understand clearly and can repay responsibly.

Disclaimer

The information in this article is for educational purposes only and should not be considered financial, legal, tax, credit, loan, or investment advice. Personal loan rates, credit card APRs, fees, repayment terms, rewards, approval requirements, and lender or card issuer policies may change over time. Always review the official terms and disclosures from the lender or card issuer before applying for or using any financial product. If you have questions about your personal financial situation, consider speaking with a qualified professional.

Leave a Reply