Personal loans can be useful when you need to borrow money for a planned expense, emergency cost, debt consolidation, home repair, medical bill, or other personal financial need.

But before accepting a personal loan, beginners should understand the fees.

A loan may look affordable at first because the monthly payment seems reasonable. However, fees can increase the total cost of borrowing. Some fees may be charged upfront, while others may apply only if you miss a payment, pay late, return a payment, or pay off the loan early.

Understanding common personal loan fees can help you compare offers more clearly and avoid surprises.

Why Loan Fees Matter

Loan fees matter because they can change the real cost of borrowing.

When comparing personal loans, many beginners focus only on the interest rate or monthly payment. These numbers are important, but they do not always show the full cost.

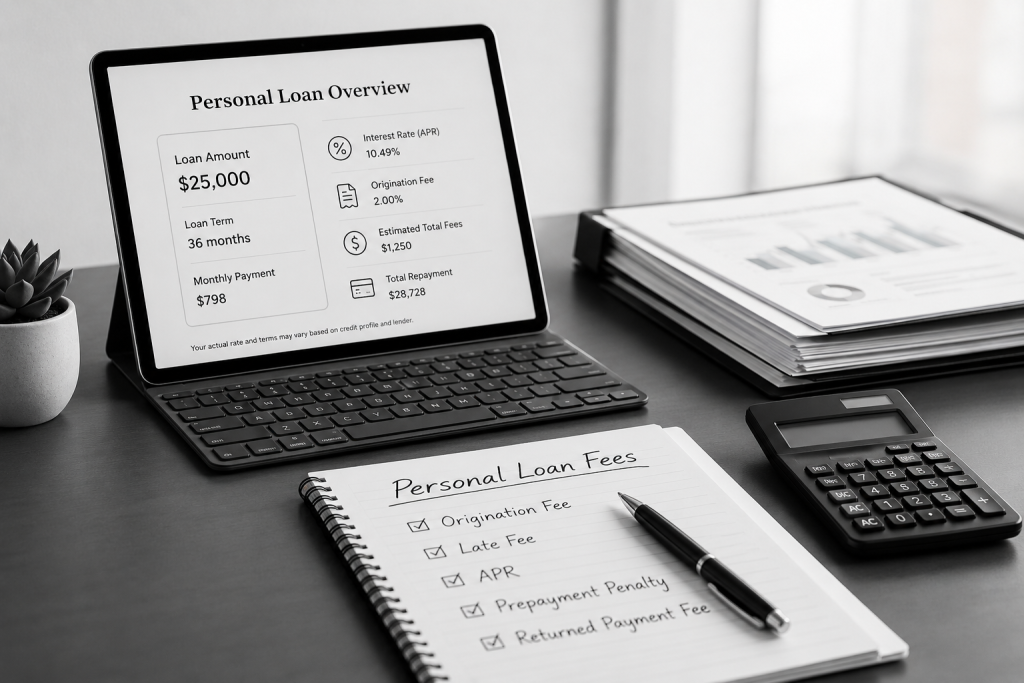

A personal loan may include fees such as origination fees, late payment fees, returned payment fees, processing fees, or prepayment penalties.

For example, two loans may have the same interest rate, but one loan may charge a large origination fee while the other does not.

This is why you should review the loan agreement and fee schedule carefully before accepting any loan.

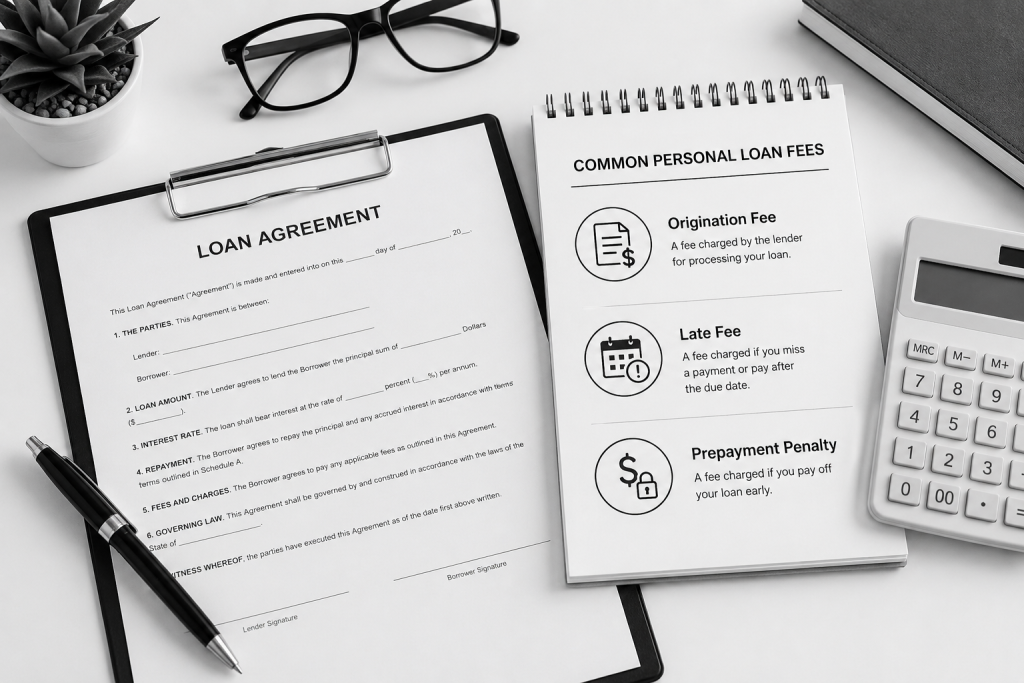

Origination Fees

An origination fee is one of the most common personal loan fees.

It is a fee some lenders charge for processing or issuing the loan.

The origination fee may be a flat amount or a percentage of the loan amount.

For example, if you borrow $10,000 and the lender charges a 5 percent origination fee, the fee would be $500.

This fee may be deducted from the loan amount before you receive the money, or it may be included in the total loan cost.

If the fee is deducted upfront, you may receive less money than expected.

For example, if you are approved for a $10,000 loan with a $500 origination fee deducted from the funds, you may receive $9,500.

This is important because you may need to borrow more to receive the amount you actually need.

Before accepting a loan, check whether there is an origination fee, how much it is, and how it is charged.

Late Payment Fees

A late payment fee may apply if you do not make your loan payment by the due date.

This fee can make the loan more expensive and may also lead to other problems.

Missing payments may affect your credit, create stress, and make it harder to manage your finances.

Before accepting a loan, check:

- How much the late payment fee is

- When the fee applies

- Whether there is a grace period

- How late payments are reported

- What happens after multiple missed payments

Some lenders may offer a short grace period, while others may charge a fee quickly after the due date.

The best way to avoid late fees is to set reminders, use automatic payments carefully, and keep enough money available before the payment date.

Prepayment Penalties

A prepayment penalty is a fee some lenders may charge if you pay off your loan early.

Not every personal loan has a prepayment penalty, but beginners should always check.

Paying off a loan early can sometimes save money on interest. However, if the loan has a prepayment penalty, that fee may reduce the benefit of early repayment.

For example, if you plan to pay off your loan faster after your income improves, a prepayment penalty could make that strategy less useful.

Before accepting a loan, ask whether you can pay extra or pay off the loan early without a penalty.

A loan with no prepayment penalty may give you more flexibility.

Returned Payment Fees

A returned payment fee may apply when your loan payment cannot be processed.

This may happen if your bank account does not have enough money, your account information is incorrect, or the payment is rejected.

A returned payment can create multiple problems.

You may be charged by the lender. Your bank may also charge a separate fee. The missed payment may still need to be paid, and late fees may apply if the issue is not fixed quickly.

To avoid returned payment fees, make sure your payment account is correct and that you have enough funds before the payment date.

If you use automatic payments, check your account before the scheduled payment.

Application Fees

Some lenders may charge an application fee.

An application fee is a fee charged just to apply for the loan or have your application reviewed.

Many personal loan lenders do not charge application fees, but some may.

Beginners should be careful with application fees because paying a fee does not always mean you will be approved.

Before applying, check whether the lender charges an application fee and whether the fee is refundable.

If a lender asks for unusual upfront payments before approval, be cautious and review the lender carefully.

Processing or Administrative Fees

Some lenders may use terms like processing fee, administrative fee, document fee, or service fee.

These fees may be charged for handling paperwork, preparing documents, managing the loan, or processing the application.

Sometimes these fees are separate. Sometimes they are included in an origination fee.

Before accepting a loan, review the full fee schedule and ask the lender to explain any fee you do not understand.

A small fee may not seem important, but multiple small fees can add up.

APR vs Fees

APR stands for Annual Percentage Rate.

APR can help you understand the cost of borrowing because it may include the interest rate and certain fees.

For personal loans, APR is often more useful than interest rate alone because it gives a broader view of the loan cost.

However, APR may not include every possible fee.

For example, late fees or returned payment fees may not be included because they only apply if something goes wrong.

This means you should look at both APR and the full fee schedule.

Do not assume a loan is cheap only because the interest rate looks low.

A loan with a lower interest rate but higher fees may cost more than another loan with a slightly higher interest rate and fewer fees.

How Fees Affect the Total Cost of a Loan

Fees can affect the total cost of a loan in several ways.

Some fees reduce the amount of money you receive.

Some fees increase the amount you repay.

Some fees only apply if you miss a payment or break a loan rule.

For example, an origination fee may reduce the amount you receive upfront.

Late payment fees can add extra costs if you miss due dates.

A prepayment penalty can make early repayment more expensive.

Returned payment fees can happen if your bank payment fails.

When comparing loans, you should look at the total repayment cost, not just the loan amount.

The total repayment cost includes the money you borrowed, interest, and applicable fees.

How to Compare Loan Fees Before Applying

Before applying for a personal loan, compare the fees from different lenders.

Look at:

- Origination fee

- Late payment fee

- Returned payment fee

- Prepayment penalty

- Application fee

- Processing fee

- Administrative fee

- APR

- Monthly payment

- Total repayment cost

Try to compare loans with the same loan amount and similar repayment terms.

For example, comparing a $10,000 loan for three years from different lenders can help you see which offer is more affordable.

If one lender charges an origination fee and another does not, check how that changes the amount you receive and the total cost.

Also read the fine print before accepting the loan.

What to Ask the Lender

Before accepting a loan, ask clear questions.

You can ask:

- Is there an origination fee?

- Will the fee be deducted from the loan amount?

- Are there late payment fees?

- Is there a grace period?

- Is there a prepayment penalty?

- Are there returned payment fees?

- Are there application or processing fees?

- What is the APR?

- What is the total repayment cost?

- Can I see the full loan agreement before accepting?

A trustworthy lender should provide clear answers.

If a lender avoids explaining fees or pressures you to accept quickly, be careful.

Common Beginner Mistakes to Avoid

One common mistake is looking only at the monthly payment.

A low monthly payment may feel comfortable, but the loan may still cost more over time if the term is long or fees are high.

Another mistake is ignoring the origination fee.

If the fee is deducted upfront, you may receive less money than expected.

Some beginners also forget to check for prepayment penalties. This matters if you want the option to pay off the loan early.

Another mistake is not reading the loan agreement.

Advertisements may show simple numbers, but the full agreement explains the real terms.

It is also a mistake to borrow more than needed just because the lender offers a larger amount.

Borrowing more usually means paying more interest and possibly more fees.

How to Avoid Unnecessary Loan Fees

You can reduce unnecessary loan fees by comparing lenders carefully and managing payments responsibly.

Choose a loan with clear terms.

Avoid loans with confusing or excessive fees.

Set payment reminders before the due date.

Keep enough money in your bank account for payments.

Consider automatic payments only if you can manage your account balance.

Avoid borrowing more than you need.

Check whether early repayment is allowed without a penalty.

Read every part of the loan agreement before accepting.

The goal is not only to get approved. The goal is to borrow in a way that is affordable and manageable.

Final Thoughts

Personal loan fees can make a loan more expensive than it first appears.

Beginners should understand common fees such as origination fees, late payment fees, prepayment penalties, returned payment fees, application fees, processing fees, and administrative fees.

Before accepting a personal loan, compare APR, monthly payment, loan term, total repayment cost, and all possible fees.

Do not choose a loan only because the monthly payment looks low or the approval process seems easy.

A good loan should have clear terms, reasonable costs, and a payment you can afford.

Disclaimer

The information in this article is for educational purposes only and should not be considered financial, legal, tax, credit, loan, or investment advice. Personal loan fees, APRs, interest rates, repayment terms, approval requirements, and lender policies may change over time. Always review the official loan agreement and disclosures from the lender before applying for or accepting any loan. If you have questions about your personal financial situation, consider speaking with a qualified professional.

Leave a Reply