Choosing your first credit card can feel confusing. There are many card types, reward programs, interest rates, fees, and promotional offers to compare. For beginners, one of the simplest choices is often a no annual fee credit card.

A no annual fee credit card is exactly what it sounds like: a credit card that does not charge a yearly fee just to keep the account open. This can make it easier for beginners to build credit without adding an extra cost.

However, no annual fee does not automatically mean the card is perfect. You still need to understand the APR, rewards, credit limit, late fees, and card terms before applying.

This guide explains how no annual fee credit cards work, why they can be helpful for beginners, and what to watch out for.

What Is a No Annual Fee Credit Card?

A no annual fee credit card is a card that does not charge a yearly membership fee.

Some credit cards charge an annual fee because they offer premium benefits, travel perks, higher rewards, airport lounge access, or special services. These cards may be useful for some people, but they are not always the best choice for beginners.

With a no annual fee card, you can usually keep the account open without paying a yearly cost. This is useful because credit history can become more valuable over time. Keeping an older account open may help your credit profile, especially if the card is managed responsibly.

For beginners, the main advantage is simple: you can focus on building good credit habits without worrying about whether the card’s benefits are worth an annual fee.

Why Beginners Often Choose No Annual Fee Cards

No annual fee cards are popular with beginners because they are simple and low-cost.

When you are new to credit, your main goal should not be getting the most complicated rewards system. Your main goal should be learning how to use credit responsibly.

A no annual fee card can help with that because it reduces the pressure to “get value” from the card.

For example, if a card charges a $95 annual fee, you may feel like you need to spend more or use certain benefits just to justify the cost. That can lead to unnecessary spending.

With a no annual fee card, there is less pressure. You can use the card for small purchases, pay the bill on time, and build credit slowly.

That makes this type of card beginner-friendly.

The Main Benefits of No Annual Fee Credit Cards

There are several reasons a no annual fee card can be a good starting point.

First, there is no yearly cost to keep the card open. This is helpful if you want to build credit without paying extra money.

Second, these cards are often easier to understand. Many no annual fee cards offer simple cash back or basic rewards. Some may not offer many rewards at all, but they can still be useful for building credit.

Third, no annual fee cards can be easier to keep long term. Since there is no yearly cost, you may be more comfortable keeping the account open even if you do not use it often.

Fourth, they can help beginners focus on the most important credit habits: paying on time, keeping balances low, and avoiding unnecessary debt.

For many beginners, simple is better.

No Annual Fee Does Not Mean No Cost

This is very important: no annual fee does not mean the card is completely free in every situation.

You may still pay other costs if you use the card incorrectly.

Possible costs can include:

- Interest charges if you carry a balance

- Late payment fees

- Foreign transaction fees

- Cash advance fees

- Balance transfer fees

- Penalty APR

- Returned payment fees

This is why beginners should not choose a card based only on the phrase “no annual fee.”

You still need to read the card’s terms and understand how the card works.

If you pay your full statement balance on time every month, you can usually avoid interest on purchases. But if you carry a balance, interest charges may become much more expensive than any rewards you earn.

APR Still Matters

APR stands for Annual Percentage Rate. It is the interest rate you may pay if you carry a balance on your credit card.

Even a no annual fee card can have a high APR.

This matters because the card may look inexpensive at first, but it can become costly if you do not pay your balance in full.

For example, a card may have no annual fee and offer cash back. But if you carry a balance and pay interest every month, the interest may cost much more than the rewards are worth.

That is why the best strategy is to use the card only for purchases you can afford to repay.

A no annual fee card works best when you use it responsibly and avoid carrying debt.

Rewards Can Be Simple

Many no annual fee cards offer simple rewards, such as cash back on everyday purchases.

For beginners, simple rewards are usually easier to manage than complicated reward programs. A flat cash back card, for example, may give the same percentage back on most purchases. That is easier to understand than a card with rotating categories, travel points, or complex redemption rules.

However, rewards should never be the main reason you overspend.

A good rule is this: only earn rewards on purchases you were already going to make.

If you buy things just to get cash back, you are not really saving money.

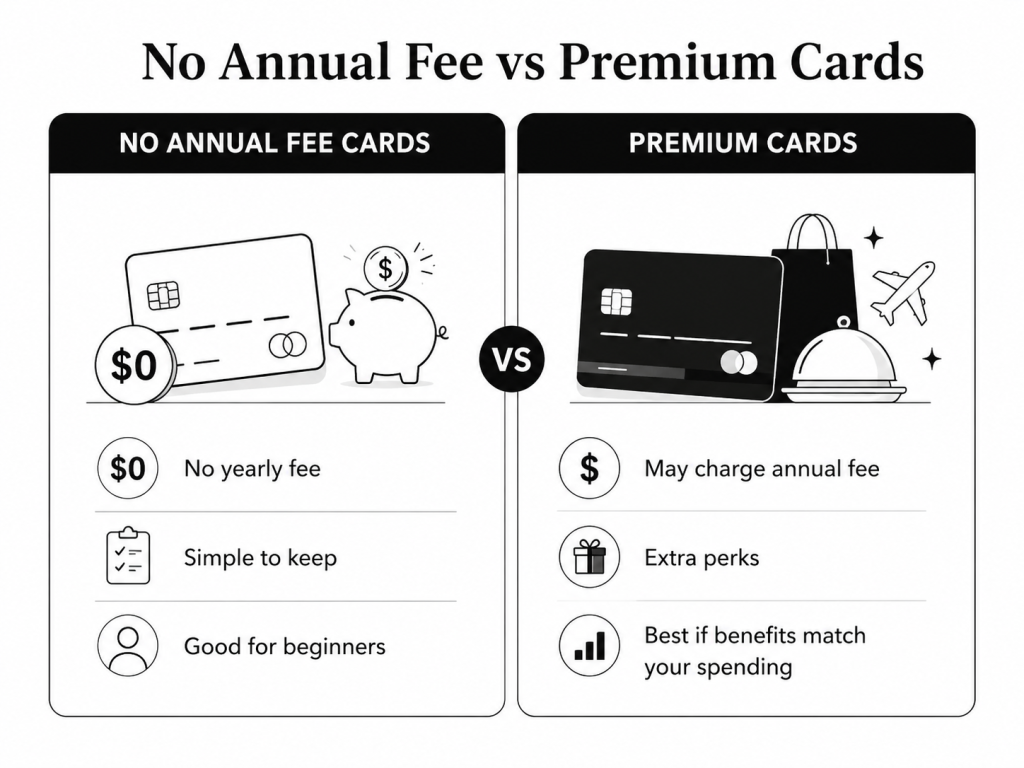

No Annual Fee vs Premium Credit Cards

Premium credit cards may offer travel credits, lounge access, higher rewards, insurance benefits, or luxury perks. Some people can get real value from these cards, especially if they travel often or use the benefits regularly.

But premium cards often charge annual fees.

For beginners, premium cards can be harder to manage. You need to understand whether the benefits are actually worth the cost. If you do not use the benefits, the annual fee may become wasted money.

No annual fee cards are usually simpler.

They may not offer the highest rewards or luxury benefits, but they can be a better starting point for someone who is learning how credit works.

A premium card may be useful later. But in the beginning, a simple no annual fee card is often enough.

Who Should Consider a No Annual Fee Credit Card?

A no annual fee card may be a good fit if you are new to credit cards, trying to build credit, or want a simple card for everyday purchases.

It may also be useful if you want to keep a credit account open long term without paying a yearly fee.

This type of card may be especially helpful for:

- First-time credit card users

- Students

- People building credit history

- People who want a backup card

- People who do not want travel perks

- People who prefer simple cash back

- People who want to avoid unnecessary fees

A no annual fee card may not be the best fit if you travel often and can fully use premium card benefits. But for many beginners, it is a practical choice.

What to Check Before Applying

Before applying for a no annual fee credit card, check more than just the annual fee.

Look at the APR. If you might carry a balance, this is very important.

Check the late payment fee. Paying late can cost money and may hurt your credit.

Check the rewards program. Make sure it is simple and useful for your normal spending habits.

Check foreign transaction fees if you travel or buy from international websites.

Check the credit score requirements if they are available.

Review whether the issuer reports to the major credit bureaus. This is important if your goal is building credit.

Also check whether the card has a grace period. A grace period can help you avoid interest if you pay your statement balance in full by the due date.

Common Mistakes Beginners Should Avoid

One mistake is choosing a card only because it has no annual fee. That is a good feature, but it is not the only thing that matters.

Another mistake is ignoring APR. If you carry a balance, APR can become expensive.

Some beginners also apply for too many cards too quickly. This can make your credit profile look risky and may affect your credit score.

Another common mistake is treating the credit limit like extra income. A credit limit is borrowed money, not free money.

Beginners should also avoid using a credit card for purchases they cannot afford to repay.

The safest approach is to keep spending small, pay on time, and avoid carrying a balance.

How to Use a No Annual Fee Card Wisely

A simple strategy is to use the card for small regular purchases, such as gas, groceries, or a monthly subscription.

Then pay the full balance every month.

You can set payment reminders or automatic payments to avoid missing a due date. If possible, pay more than the minimum payment. Paying only the minimum can lead to long-term debt if you carry a balance.

Try to keep credit utilization low. Credit utilization means how much of your available credit you are using. Many beginners try to keep utilization below 30%, and lower may be even better.

For example, if your credit limit is $1,000, try not to let your balance stay above $300.

Using the card carefully can help you build positive credit habits over time.

Are No Annual Fee Cards Always Better?

No annual fee cards are often better for beginners, but they are not always better for everyone.

If you are an experienced credit card user and you know how to use premium benefits, a card with an annual fee may sometimes provide more value.

For example, if a premium card offers travel benefits that you use every year, the value may be higher than the annual fee.

But if you are not using those benefits, the fee may not be worth it.

For beginners, a no annual fee card is usually the safer and simpler starting point.

Final Thoughts

No annual fee credit cards can be a smart choice for beginners because they are simple, low-cost, and easier to keep long term.

They can help you build credit without paying a yearly fee. They can also make it easier to focus on responsible habits, such as paying on time and keeping balances low.

However, no annual fee does not mean there are no possible costs. You still need to understand APR, late fees, rewards, and card terms.

If you are new to credit cards, start simple. Choose a card you understand, use it carefully, and pay your balance on time.

A no annual fee card may not be the most exciting card, but it can be one of the best starting points for building a strong financial foundation.

Disclaimer

The information in this article is for educational purposes only and should not be considered financial, legal, tax, credit, or investment advice. Credit card terms, fees, rewards, interest rates, and approval requirements may change over time. Always review the official terms and disclosures from the credit card issuer before applying or using any credit card. If you have questions about your personal financial situation, consider speaking with a qualified professional.

Leave a Reply