What Is APR and Why Does It Matter?

If you are new to credit cards, one of the most important terms to understand is APR. Many beginners focus only on rewards, cash back, or sign-up bonuses, but APR can have a much bigger impact on your money if you carry a balance.

APR stands for Annual Percentage Rate. It represents the yearly cost of borrowing money, expressed as a percentage.

In simple terms, APR tells you how expensive it can be to borrow money on your credit card if you do not pay your balance in full.

Understanding APR can help you avoid unnecessary interest, compare credit cards more carefully, and use credit responsibly.

What Is APR?

APR means Annual Percentage Rate. It is the interest rate you may pay over a year when you borrow money.

For credit cards, APR usually applies when you carry a balance from one billing cycle to the next. If you pay your full statement balance by the due date, you can usually avoid paying interest on purchases.

But if you do not pay the full balance, the credit card issuer may charge interest based on your APR.

For example, if your credit card has a high APR and you leave a balance unpaid, the cost can grow quickly over time.

This is why APR matters, especially for beginners.

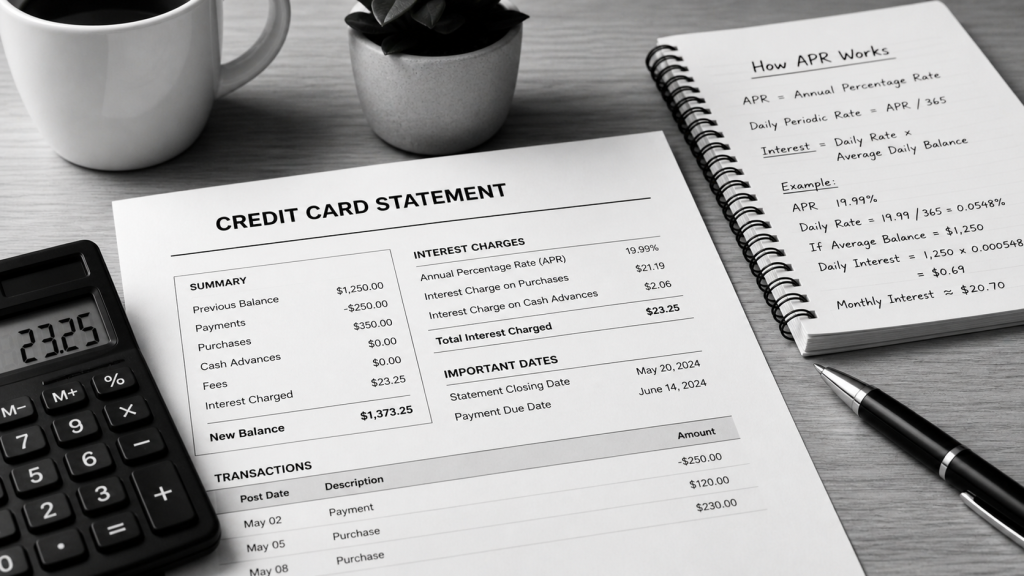

How Credit Card APR Works

Credit card APR is shown as a yearly rate, but interest is usually calculated more frequently, often daily.

That means your card issuer may convert the annual APR into a daily periodic rate and apply it to your unpaid balance.

You do not need to memorize the formula to use a credit card wisely. The main idea is simple:

The longer you carry a balance, the more interest you may pay.

For example, if you make a purchase and pay it off in full by the due date, you may pay no interest. But if you carry that purchase into the next billing cycle, interest may begin to apply.

Even small purchases can become more expensive if they remain unpaid for a long time.

A Simple APR Example

Imagine you use your credit card to buy something for $100.

If you pay the full $100 by the due date, you usually do not pay interest.

But if you only pay part of the balance and leave the rest unpaid, your credit card issuer may charge interest on the remaining amount.

Now imagine this happens month after month. A balance that starts small can become more expensive because interest keeps adding up.

This is why credit cards can be helpful tools when used responsibly, but costly when used like long-term loans.

APR vs Annual Fee

APR and annual fee are not the same thing.

An annual fee is a fixed fee you may pay once a year just to keep the card open.

APR is the interest rate you may pay if you carry a balance.

A card can have no annual fee but still have a high APR. Another card may have an annual fee but offer rewards or benefits. For beginners, it is usually smart to focus on simple cards with low costs and clear terms.

If you plan to pay your balance in full every month, APR may not affect you as much. But if you think you might carry a balance, APR becomes very important.

Why APR Matters for Beginners

APR matters because it shows the potential cost of borrowing.

Many new credit card users think mostly about rewards, such as points or cash back. But rewards are usually small compared to the interest you may pay if you carry a balance.

For example, earning 1% or 2% cash back does not help much if you are paying a much higher interest rate on unpaid balances.

This is one of the biggest mistakes beginners make.

Rewards are useful only when you are not paying more in interest and fees than you earn back.

Different Types of APR

Credit cards may have different APRs for different situations. When comparing cards, you may see terms like:

Purchase APR

This is the APR applied to regular purchases if you carry a balance.

Balance Transfer APR

This may apply when you move debt from one credit card to another. Some cards offer promotional balance transfer APRs, but fees and deadlines may apply.

Cash Advance APR

This applies when you use your credit card to withdraw cash. Cash advances often have higher APRs and additional fees, so beginners should be very careful with them.

Penalty APR

Some issuers may charge a higher penalty APR if you miss payments or violate card terms. This can make debt much more expensive.

Introductory APR

Some cards offer a low or 0% introductory APR for a limited time. This can be helpful, but only if you understand when the promotional period ends and what the regular APR will be afterward.

How to Find a Credit Card’s APR

Credit card issuers are required to show important pricing information before you apply. You can usually find APR details in the card’s terms and conditions or pricing table.

Before applying for a card, look for:

- Purchase APR

- Annual fee

- Late payment fee

- Balance transfer APR

- Cash advance APR

- Penalty APR

- Introductory APR terms

- Grace period information

Do not rely only on marketing headlines. Always read the official terms from the card issuer.

How to Avoid Paying Credit Card Interest

The best way to avoid credit card interest is to pay your statement balance in full by the due date every month.

Here are a few simple habits:

- Use your card only for purchases you can afford.

- Track your spending during the month.

- Set up payment reminders or automatic payments.

- Pay more than the minimum payment.

- Avoid cash advances.

- Keep your credit utilization low.

- Review your statement before the due date.

If you only make the minimum payment, it may take a long time to pay off your balance, and interest can become expensive.

Common APR Mistakes to Avoid

Many beginners make the same mistakes when it comes to APR.

One common mistake is ignoring APR because the card offers rewards. Rewards are not worth much if interest charges are higher than the cash back or points you earn.

Another mistake is assuming a 0% APR offer lasts forever. Introductory offers usually expire, and the regular APR may be much higher.

Some users also treat the credit limit like extra income. A credit limit is not free money. It is borrowed money that must be repaid.

Another mistake is paying only the minimum amount each month. This keeps the account open, but it can make the debt last much longer.

APR and Credit Score

APR can also be connected to your credit profile. People with stronger credit histories may qualify for better rates and better credit card offers.

If you are new to credit, your APR may be higher at first. That does not mean you should avoid credit cards completely. It means you should use them carefully.

Paying on time, keeping balances low, and building a positive credit history can help improve your financial profile over time.

Final Thoughts

APR is one of the most important credit card terms beginners should understand. It tells you how expensive borrowing can become if you do not pay your balance in full.

A credit card can help you build credit, earn rewards, and manage purchases. But if you carry a balance, APR can make your purchases more expensive.

Before applying for any card, review the APR, fees, rewards, and terms carefully. If you already have a credit card, focus on paying on time and avoiding unnecessary interest.

The best credit card strategy is simple: use your card responsibly, pay the full balance when possible, and never spend more than you can afford to repay.

Disclaimer

This article is for educational purposes only and should not be considered financial, legal, tax, credit, or investment advice. Credit card APRs, fees, rates, and terms may change over time. Always review the official issuer terms before applying.

Leave a Reply