Opening a bank account can seem simple, but beginners should always compare fees before choosing an account.

A checking account or savings account may look free at first, but some accounts have monthly fees, overdraft fees, ATM fees, transfer fees, paper statement fees, or minimum balance requirements.

These fees may seem small, but they can add up over time.

Before opening an account, it is important to understand what fees may apply and how to avoid unnecessary costs.

This guide explains how to compare bank account fees step by step.

Why Account Fees Matter

Account fees matter because they can reduce the money you keep in your account.

A bank account should help you manage money, receive deposits, pay bills, save, and access funds easily.

But if the account charges frequent fees, it may become expensive.

For example, a monthly maintenance fee may not seem like much, but it can cost a lot over a full year.

Overdraft fees can also become expensive if you spend more than your balance.

ATM fees may add up if you often use machines outside your bank’s network.

Comparing fees before opening an account can help you:

- Avoid unnecessary charges

- Choose a better account

- Understand account rules

- Protect your savings

- Manage money more easily

- Reduce surprises

- Build better banking habits

For beginners, a simple low-fee account is often easier to manage.

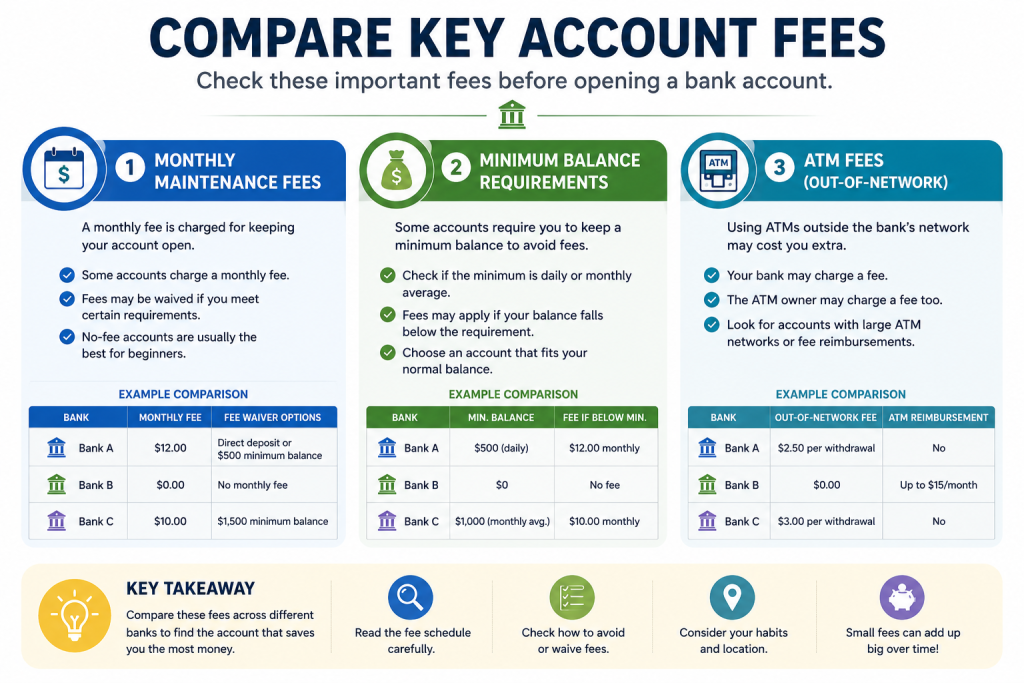

Start With Monthly Maintenance Fees

A monthly maintenance fee is a fee some banks charge just for keeping the account open.

This fee may apply to checking accounts, savings accounts, or money market accounts.

Some accounts have no monthly fee. Others may charge a fee unless you meet certain requirements.

Common ways to waive monthly fees may include:

- Keeping a minimum balance

- Setting up direct deposit

- Making a certain number of transactions

- Linking another account

- Being a student

- Meeting age-based requirements

- Using paperless statements

Before opening an account, check whether there is a monthly fee.

Then ask:

- How much is the fee?

- Can the fee be waived?

- Can I realistically meet the waiver requirement?

- What happens if I miss the requirement one month?

If you are not sure you can meet the requirement every month, a no-monthly-fee account may be a better choice.

Check Minimum Balance Requirements

Some accounts require you to keep a minimum balance.

A minimum balance is the amount of money you must keep in the account to avoid fees or keep certain benefits.

For example, an account may require a minimum daily balance or an average monthly balance.

These are not always the same.

A minimum daily balance means your account balance must stay above a certain amount every day.

An average monthly balance means the bank calculates your average balance during the month.

Before opening an account, check:

- Is there a minimum balance requirement?

- Is it daily or monthly average?

- What fee applies if I fall below the minimum?

- Do I need this balance to earn interest?

- Do I need this balance to avoid monthly fees?

For beginners, high minimum balance requirements can be difficult to maintain.

If your balance changes often, choose an account with low or no minimum balance requirements.

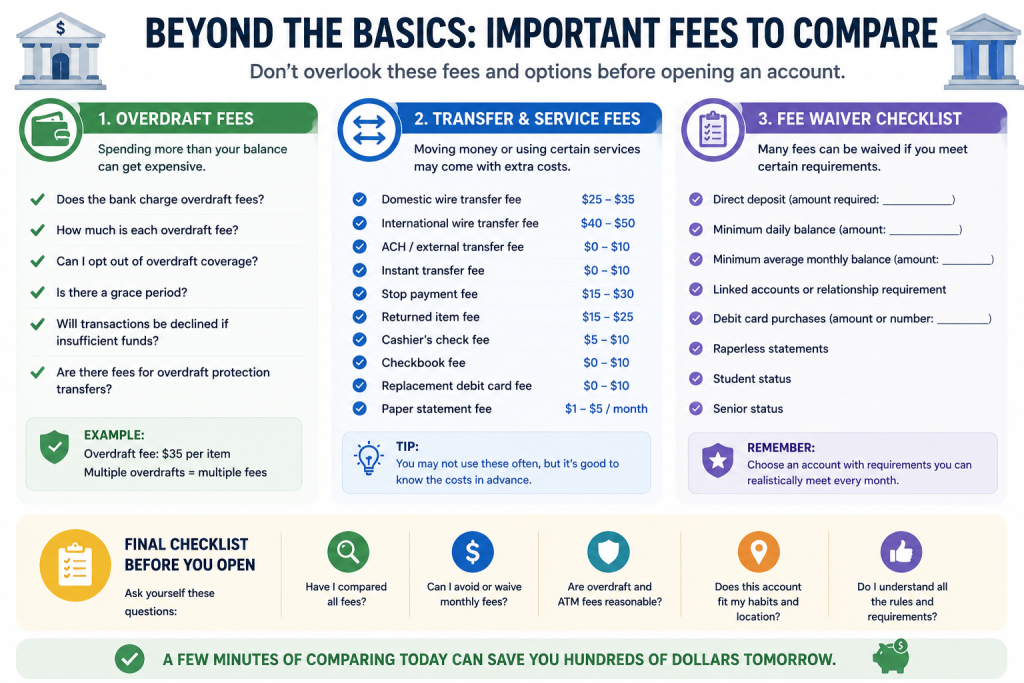

Understand Overdraft Fees

Overdraft fees can happen when you spend more money than you have available in your account.

For example, if your account balance is $20 and a payment of $50 goes through, your account may become negative.

Some banks may charge an overdraft fee.

Overdraft fees can be expensive, especially if multiple transactions cause multiple fees.

Before opening an account, review the overdraft rules carefully.

Check:

- Does the bank charge overdraft fees?

- How much is each overdraft fee?

- Can I opt out of overdraft coverage?

- Does the bank offer overdraft protection?

- Are there transfer fees for overdraft protection?

- Is there a grace period?

- Will transactions be declined if there is not enough money?

Some beginners may prefer an account that declines transactions instead of allowing overdrafts.

This can help avoid expensive fees.

Compare ATM Fees

ATM access is important if you often withdraw cash.

Banks may offer free access to certain ATMs, but they may charge fees when you use out-of-network ATMs.

Sometimes, both your bank and the ATM owner may charge fees.

Before opening an account, check:

- How large is the ATM network?

- Are there free ATMs near me?

- Does the bank charge out-of-network ATM fees?

- Does the bank reimburse ATM fees?

- Are international ATM fees different?

- Are there limits on ATM withdrawals?

If you rarely use cash, ATM fees may not matter much.

But if you withdraw cash often, ATM access can be very important.

Look for Transfer and Wire Fees

Transfer fees may apply when moving money between accounts or sending money to another person or institution.

Common transfer-related fees may include:

- Domestic wire transfer fees

- International wire transfer fees

- ACH transfer fees

- External transfer fees

- Instant transfer fees

- Stop payment fees

- Returned transfer fees

Many standard transfers may be free, but faster or special transfers may cost money.

Before opening an account, check how you plan to move money.

Ask:

- Will I transfer money to other banks?

- Will I send wires?

- Will I need international transfers?

- Will I use instant transfers?

- Are there transfer limits?

- Are there transfer fees?

If you often move money between accounts, transfer fees and limits should be reviewed carefully.

Check Paper Statement and Service Fees

Some banks charge fees for paper statements or certain account services.

These fees are easy to miss because they may not be part of the main account advertisement.

Possible service fees may include:

- Paper statement fees

- Checkbook fees

- Cashier’s check fees

- Money order fees

- Stop payment fees

- Account research fees

- Replacement debit card fees

- Returned deposit fees

- Dormant account fees

You may not use these services often, but it is still helpful to know the costs.

If you prefer paper statements, check whether the bank charges for them.

If you are comfortable with online banking, choosing paperless statements may help avoid fees.

Review Account Closing Fees

Some banks may charge a fee if you close an account too soon after opening it.

This is sometimes called an early account closure fee.

For example, a bank may charge a fee if you close the account within a certain number of days or months.

Before opening an account, check:

- Is there an early closure fee?

- How long do I need to keep the account open?

- What happens if I close it early?

- Are there rules tied to a sign-up bonus?

This is especially important if the account offers a promotional bonus.

Some bonuses require the account to remain open for a certain period.

Compare Fee Waiver Options

Some accounts have fees, but those fees can be waived if you meet certain conditions.

Fee waiver options can be useful, but only if they fit your real habits.

Common fee waiver conditions include:

- Direct deposit

- Minimum daily balance

- Minimum average balance

- Linked accounts

- Debit card activity

- Student status

- Senior status

- Paperless statements

Before relying on a fee waiver, ask:

- Can I meet this requirement every month?

- Is the requirement easy or stressful?

- Will my income or balance change?

- Is there a no-fee account available instead?

A fee waiver is helpful only if it is realistic.

If the requirement is hard to meet, the account may still become expensive.

Choose an Account That Fits Your Habits

The best bank account is not the same for everyone.

Your habits should guide your choice.

If you use cash often, choose an account with good ATM access.

If you keep a low balance, avoid accounts with high minimum balance requirements.

If you receive regular paychecks, direct deposit may help waive fees.

If you travel often, review ATM and foreign transaction fees.

If you prefer online banking, compare mobile app features, alerts, and online transfers.

If you want simple banking, choose an account with fewer fees and clear rules.

A bank account should fit how you actually manage money.

Do not choose an account only because of a bonus, advertisement, or brand name.

Compare Checking and Savings Account Fees

Checking accounts and savings accounts may have different fee structures.

Checking accounts are usually used for everyday transactions, debit card purchases, bill payments, ATM withdrawals, and direct deposit.

Savings accounts are usually used to store money for future needs.

Checking account fees may include:

- Monthly maintenance fees

- Overdraft fees

- ATM fees

- Debit card replacement fees

- Check fees

- Wire transfer fees

Savings account fees may include:

- Monthly maintenance fees

- Minimum balance fees

- Excess withdrawal fees

- Transfer fees

- Paper statement fees

Before opening either type of account, review the account agreement and fee schedule.

A checking account should be easy to use for daily money activity.

A savings account should help you store money without unnecessary costs.

Look at Online Banks and Traditional Banks

Online banks and traditional banks may have different fee structures.

Online banks often have lower fees because they do not operate large branch networks.

They may offer no monthly fees, higher savings rates, or easier digital tools.

Traditional banks may offer branch access, in-person support, cash deposits, and larger ATM networks.

Neither option is automatically better.

Compare:

- Monthly fees

- ATM access

- Cash deposit options

- Mobile app tools

- Customer support

- Savings rates

- Transfer speed

- Branch availability

- Account requirements

If you need in-person banking, a traditional bank may be useful.

If you prefer digital banking and low fees, an online bank may be a better fit.

Read the Fee

Schedule Before Opening

The fee schedule is one of the most important documents to review.

It lists many possible charges connected to the account.

Before opening an account, find the official fee schedule from the bank or credit union.

Look for:

- Monthly fee

- Minimum balance fee

- Overdraft fee

- ATM fee

- Wire transfer fee

- Paper statement fee

- Replacement card fee

- Stop payment fee

- Returned item fee

- Account closing fee

- Dormant account fee

Do not rely only on the marketing page.

The marketing page may highlight benefits, while the fee schedule explains the real costs.

Common Beginner Mistakes

One common mistake is opening an account without reading the fee schedule.

Another mistake is choosing an account only because of a sign-up bonus.

A bonus may not be worth it if the account has fees or requirements that do not fit your situation.

Some beginners ignore minimum balance rules and later get charged monthly fees.

Others use out-of-network ATMs often and pay unnecessary charges.

Another mistake is misunderstanding overdraft rules.

Some people also forget to cancel paper statements and get charged fees.

A simple account with clear rules can help beginners avoid these mistakes.

Simple Checklist Before Opening an Account

Before opening a checking or savings account, ask:

- Is there a monthly maintenance fee?

- Can the monthly fee be waived?

- Is there a minimum balance requirement?

- Are there overdraft fees?

- Can I opt out of overdraft coverage?

- Are there free ATMs near me?

- Does the bank charge out-of-network ATM fees?

- Are there transfer or wire fees?

- Are paper statements free?

- Is there an early account closure fee?

- Does the account fit my habits?

- Can I understand the fee schedule?

If the account has too many fees or confusing rules, keep comparing.

Final Thoughts

Comparing fees before opening an account can help you avoid unnecessary costs and choose a better banking option.

Start by reviewing monthly maintenance fees, minimum balance requirements, overdraft fees, ATM fees, transfer fees, paper statement fees, service fees, and account closing fees.

Also compare fee waiver options and make sure they fit your real habits.

For beginners, the best account is usually simple, low-cost, easy to understand, and convenient to use.

Take time to read the fee schedule before opening an account.

A few minutes of review can help you avoid surprise fees later.

Disclaimer

The information in this article is for educational purposes only and should not be considered financial, legal, tax, credit, banking, loan, or investment advice. Bank account fees, account requirements, overdraft rules, ATM access, transfer limits, interest rates, and account terms may change over time. Always review the official account agreement, fee schedule, and disclosures from the bank or credit union before opening or using any account. If you have questions about your personal financial situation, consider speaking with a qualified professional.

Leave a Reply