When comparing loans, you may see the terms secured loan and unsecured loan. These two types of loans can work differently, and the difference is important for beginners to understand.

A secured loan is backed by collateral. An unsecured loan does not require collateral.

Collateral is something valuable that the lender can use as protection if the borrower does not repay the loan.

Understanding the difference between secured and unsecured loans can help you compare borrowing options, understand risk, and make better financial decisions before applying.

What Is a Secured Loan?

A secured loan is a loan that is backed by collateral.

Collateral is an asset or item of value that the borrower agrees to use as security for the loan.

If the borrower does not repay the loan according to the agreement, the lender may have the right to take the collateral, depending on the loan terms and applicable rules.

Because secured loans include collateral, they may be less risky for the lender. In some cases, this may help borrowers qualify for a loan or receive a lower interest rate.

However, secured loans also create risk for the borrower because the collateral may be at stake.

What Is an Unsecured Loan?

An unsecured loan is a loan that does not require collateral.

Instead of using an asset as security, the lender usually looks at the borrower’s credit history, income, debt level, employment, and overall financial profile.

Many personal loans, credit cards, and student loans are examples of unsecured borrowing.

Because unsecured loans do not have collateral, they may be riskier for the lender. As a result, they may have higher interest rates or stricter approval requirements, depending on the borrower and lender.

With an unsecured loan, the lender usually cannot take collateral directly in the same way as a secured loan. However, missed payments can still lead to serious consequences, such as late fees, credit score damage, collection activity, or legal action.

The Main Difference Between Secured and Unsecured Loans

The main difference is collateral.

A secured loan requires collateral.

An unsecured loan does not require collateral.

This difference affects risk, approval, interest rates, and borrower responsibility.

With a secured loan, the lender has an asset connected to the loan. If the borrower fails to repay, the lender may be able to recover some loss through the collateral.

With an unsecured loan, the lender relies more on the borrower’s promise to repay and financial profile.

For beginners, the simple way to remember it is:

Secured loan means the loan is secured by something valuable.

Unsecured loan means there is no specific collateral attached to the loan.

What Is Collateral?

Collateral is something valuable that is used to secure a loan.

Examples of collateral may include:

- A car

- A home

- A savings account

- A certificate of deposit

- Equipment

- Other valuable property

The type of collateral depends on the loan and lender.

For example, an auto loan is usually secured by the car. A mortgage is usually secured by the home. Some secured personal loans may use savings or other assets as collateral.

Collateral reduces risk for the lender, but it increases risk for the borrower. If you cannot repay the loan, you may lose the asset tied to the loan.

Before accepting a secured loan, always understand exactly what collateral is involved and what can happen if you miss payments.

Examples of Secured Loans

Common examples of secured loans include auto loans, mortgages, secured personal loans, secured credit builder loans, and some business loans.

An auto loan is secured by the vehicle. If the borrower does not repay, the lender may be able to repossess the car.

A mortgage is secured by the property. If the borrower does not make payments, the lender may eventually begin foreclosure.

A secured personal loan may be backed by money in a savings account, certificate of deposit, vehicle, or another approved asset.

Some credit builder loans may also be secured by funds held in an account until the loan is repaid.

The exact terms can vary, so borrowers should review the loan agreement carefully.

Examples of Unsecured Loans

Common examples of unsecured loans include many personal loans, credit cards, student loans, medical loans, and some debt consolidation loans.

An unsecured personal loan usually does not require the borrower to offer a car, home, or savings account as collateral.

A credit card is also unsecured in many cases. The card issuer provides a credit limit based on the borrower’s financial profile, not a specific asset.

Even though unsecured loans do not require collateral, they still must be repaid. Missing payments can damage credit and create financial problems.

Unsecured does not mean risk-free.

Pros and Cons of Secured Loans

Secured loans can have advantages and disadvantages.

Possible advantages include:

- May be easier to qualify for

- May offer lower interest rates

- May allow larger loan amounts

- May offer longer repayment terms

- Can be useful for major purchases

Possible disadvantages include:

- Collateral may be at risk

- Missed payments can lead to asset loss

- Loan agreements can be more complex

- Borrower may feel pressured by the collateral risk

- Some secured loans may include extra fees

A secured loan may be useful when the borrower understands the risk and has a clear repayment plan.

However, beginners should be careful. Losing collateral can create serious financial stress.

Pros and Cons of Unsecured Loans

Unsecured loans also have advantages and disadvantages.

Possible advantages include:

- No collateral required

- No specific asset tied to the loan

- Can be simpler for some borrowers

- Useful for personal expenses or debt consolidation

- May offer fixed monthly payments

Possible disadvantages include:

- May have higher interest rates

- May be harder to qualify for

- Approval may depend strongly on credit and income

- May have smaller loan limits

- Missed payments can still damage credit

An unsecured loan may be useful if you do not want to risk collateral. However, the cost may be higher, especially if your credit profile is weak.

Which Type of Loan Is Easier to Qualify For?

In some cases, a secured loan may be easier to qualify for because the lender has collateral as protection.

However, this does not mean approval is guaranteed.

Lenders may still review income, credit history, debt, employment, and repayment ability.

Unsecured loans may have stricter approval requirements because there is no collateral. Borrowers with stronger credit and steady income may have better chances of approval and better loan terms.

The easier option depends on the lender, the loan type, the borrower’s credit profile, income, debt level, and collateral value.

How Interest Rates May Be Different

Interest rates can be different for secured and unsecured loans.

Because secured loans include collateral, they may sometimes offer lower interest rates than unsecured loans.

But this is not always true.

The rate may also depend on your credit score, income, debt-to-income ratio, loan amount, loan term, lender, and market conditions.

Unsecured loans may have higher rates because the lender takes more risk without collateral.

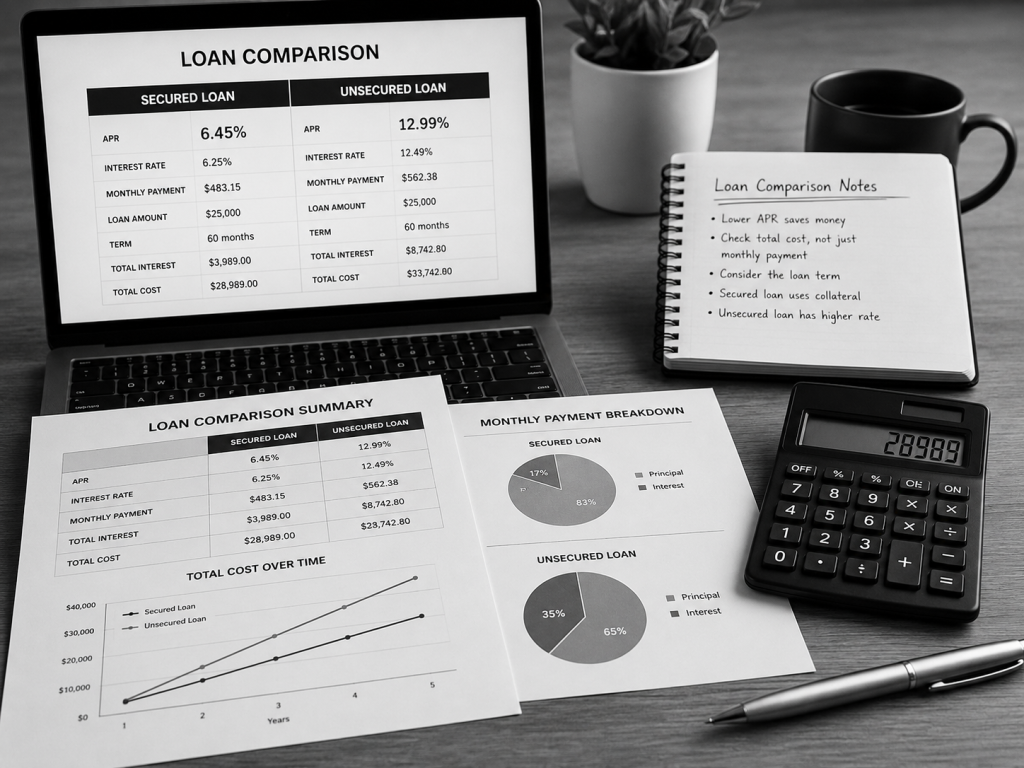

When comparing loans, do not look only at the interest rate. Also check APR, fees, loan term, monthly payment, and total repayment cost.

A loan with a lower rate may still be expensive if it has high fees or a long repayment term.

Loan Term and Monthly Payment Differences

Secured loans and unsecured loans may also have different repayment terms.

Some secured loans, such as mortgages and auto loans, may have longer repayment periods. Longer terms can lower the monthly payment, but they may increase total interest over time.

Unsecured personal loans often have shorter terms, although this depends on the lender.

When comparing options, check the monthly payment and the total cost.

A lower monthly payment may feel easier, but it can cost more over the full life of the loan if the term is long.

Beginners should make sure the payment fits their budget and that they understand the full repayment schedule.

Credit Score Impact

Both secured and unsecured loans can affect your credit.

Making payments on time may help build a positive payment history.

Missing payments may damage your credit score.

A new loan application may also create a hard inquiry, depending on the lender and application process.

The loan can also affect your credit mix, debt level, and payment history.

Whether the loan is secured or unsecured, responsible repayment matters.

Before borrowing, make sure you can afford the payment and understand how the lender reports payments to credit bureaus.

What Beginners Should Check Before Borrowing

Before choosing a secured or unsecured loan, beginners should compare several important details.

- Check whether collateral is required

- Check what happens if you miss payments

- Check the APR, not just the interest rate

- Check the loan term and monthly payment

- Check all fees, including origination fees, late fees, and prepayment penalties

- Check the total repayment cost

- Check the lender’s reputation and customer support

- Check whether the payment fits your monthly budget

- Also make sure you understand the purpose of the loan

Borrowing should solve a real financial need, not create a bigger problem.

Common Mistakes to Avoid

One common mistake is choosing a secured loan without understanding the collateral risk.

If you cannot repay the loan, losing the asset may be more serious than the original problem.

Another mistake is choosing an unsecured loan only because it does not require collateral. If the APR is high, the loan may become expensive.

Some beginners focus only on monthly payment and ignore total cost.

A longer repayment term can make the monthly payment smaller, but it may increase the total interest paid.

Another mistake is borrowing more than needed.

Whether the loan is secured or unsecured, borrowing extra money can increase financial pressure.

It is also a mistake to sign a loan agreement without reading the full terms.

Secured vs Unsecured Loan: Which Is Better?

Neither type is automatically better.

A secured loan may be better if you need a larger loan, have collateral, and can manage the repayment responsibility.

An unsecured loan may be better if you do not want to risk collateral and can qualify for reasonable terms.

The better choice depends on your financial situation, borrowing purpose, credit profile, income, debt level, and comfort with risk.

For beginners, the safest approach is to compare options carefully and choose the loan with terms you clearly understand and can afford.

Final Thoughts

Secured and unsecured loans are different because of collateral.

A secured loan is backed by something valuable, such as a car, home, savings account, or other asset.

An unsecured loan does not require collateral, but approval may depend more on credit, income, and financial history.

Both types of loans can be useful, but both can also create risk if used carelessly.

Before borrowing, compare APR, fees, monthly payment, loan term, total cost, collateral requirements, and lender reputation.

The most important rule is simple: do not borrow unless you understand the loan and have a realistic plan to repay it.

Disclaimer

The information in this article is for educational purposes only and should not be considered financial, legal, tax, credit, loan, or investment advice. Loan rates, fees, collateral requirements, approval standards, repayment terms, and lender policies may change over time. Always review the official loan agreement and disclosures from the lender before applying for or accepting any loan. If you have questions about your personal financial situation, consider speaking with a qualified professional.

Leave a Reply