Many beginners choose the wrong credit card and end up paying unnecessary fees, high interest, or using rewards they do not fully understand. The right credit card, however, can be a useful financial tool when it is chosen carefully and used responsibly.

A good beginner credit card can help you build credit history, improve your credit score over time, earn simple rewards, and prepare you for better financial opportunities in the future. But before applying for any card, it is important to understand what to look for and what to avoid.

Why Your First Credit Card Matters

Your first credit card can affect your financial profile for years. When you use a credit card responsibly, you show lenders that you can borrow money and repay it on time. This can help you build a stronger credit history.

A stronger credit history may help you qualify for loans, apartments, lower interest rates, and better financial products in the future.

But the opposite is also true. If you choose the wrong card or use it carelessly, you may pay high interest, build debt, or damage your credit score.

That is why beginners should keep things simple.

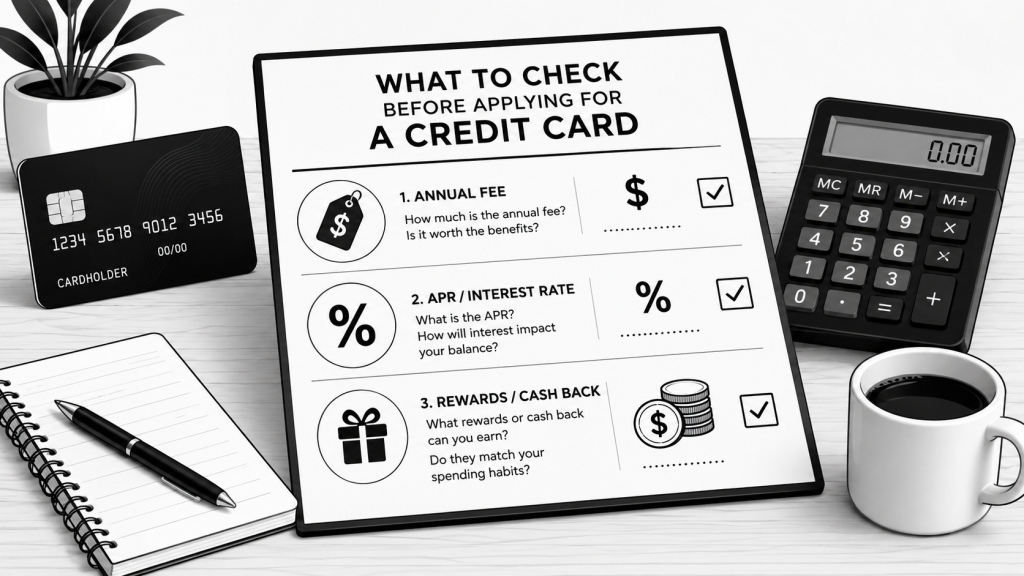

Check the Annual Fee First

Before applying for a credit card, one of the first things to check is the annual fee.

An annual fee is a fee you pay every year just to keep the card open. Some premium credit cards charge high annual fees because they offer travel benefits, luxury perks, or advanced reward systems.

For beginners, these cards are usually not the best choice.

A no-annual-fee credit card is often better for someone just starting out. It allows you to keep the card open without paying extra money every year. This makes it easier to focus on building credit without worrying about whether the card is worth the cost.

A no-annual-fee card is simple, low-risk, and easier to manage.

Understand the Interest Rate

The second thing to check is the interest rate, often called APR.

APR stands for Annual Percentage Rate. It tells you how much interest you may pay if you carry a balance from month to month.

If you pay your full balance every month, you usually do not pay interest. But if you only make the minimum payment and leave a balance on the card, interest can become expensive very quickly.

This is one of the biggest mistakes beginners make.

A credit card should not be treated like free money. If you spend more than you can afford to repay, the interest can turn small purchases into long-term debt.

For beginners, the safest rule is simple:

Only spend what you can fully pay back each month.

Choose Simple Rewards

Many credit cards offer rewards, such as points, miles, or cash back. Rewards can be useful, but they can also be confusing for beginners.

Some cards have complicated reward categories, rotating bonuses, travel rules, or redemption systems. These may be valuable for experienced users, but they are not always ideal for someone getting their first card.

For beginners, a simple cash back card is often the easiest choice.

Cash back means you earn a small percentage back when you spend. For example, if your card gives 1% to 2% cash back, you may earn $1 to $2 back for every $100 you spend.

It may not seem like much at first, but over time it can add up. More importantly, cash back is easy to understand.

If you are new to credit cards, simple rewards are better than complicated rewards.

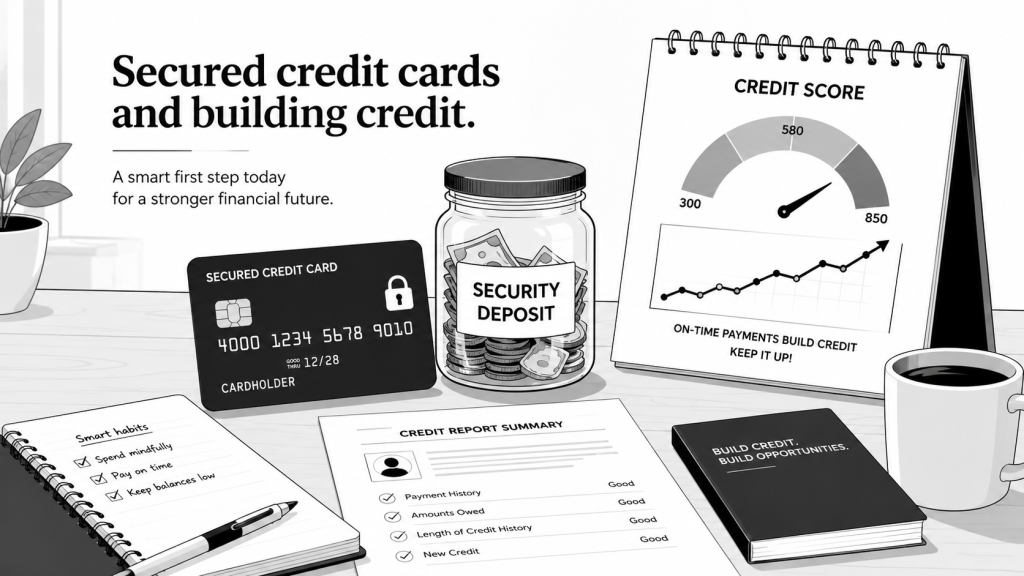

Consider a Secured Credit Card

If you have no credit history or a low credit score, you may not qualify for many regular credit cards. In that case, a secured credit card can be a good starting point.

A secured credit card usually requires a refundable security deposit. That deposit often becomes your credit limit.

For example, if you deposit $300, your credit limit may be $300.

You can then use the card for small purchases and pay the balance on time each month. Over time, responsible use may help you build credit history. After several months, some issuers may allow you to upgrade to a regular unsecured credit card.

A secured card can be one of the safest ways to begin building credit.

Avoid Common Beginner Mistakes

Choosing a credit card is not just about finding the card with the best-looking design or biggest advertisement. Beginners should avoid common mistakes that can create problems later.

Avoid cards with high annual fees unless you clearly understand the benefits and know they are worth the cost.

Avoid complicated reward programs if you do not know how to use them.

Avoid applying for too many credit cards at once. Multiple applications can affect your credit and may make lenders see you as risky.

Avoid choosing a card only because of marketing, social media hype, or a sign-up bonus.

Focus on long-term value, not short-term excitement.

Use Your Credit Card Responsibly

Choosing the right credit card is only the first step. The way you use the card matters even more.

A good beginner strategy is to start with one card and use it for small, regular purchases. For example, you can use it for groceries, gas, or a small monthly subscription.

Then pay the full balance every month.

Try to keep your credit utilization below 30%. Credit utilization means how much of your available credit you are using.

For example, if your credit limit is $1,000, try not to use more than $300 at a time.

Using too much of your available credit can hurt your credit score, even if you make payments on time.

The best habits are:

- Pay on time every month.

- Pay the full balance when possible.

- Keep credit utilization low.

- Use the card regularly but carefully.

- Avoid spending more just to earn rewards.

A Simple Beginner Credit Card Strategy

If you are new to credit cards, do not make the process complicated.

Start with one beginner-friendly credit card. Choose a no-annual-fee card if possible. Use it for small purchases. Pay it off in full every month. Keep your balance low.

After six months, review your progress. If your credit score has improved and you understand how credit cards work, you can decide whether you need another card.

Building credit takes time. Slow and steady is better than rushing.

Final Thoughts

The right credit card can help you build credit, earn simple rewards, and create better financial opportunities. But the wrong card can lead to fees, interest, and debt.

For beginners in the USA, the best credit card is usually simple, low-cost, and easy to manage.

Look for no annual fee, simple rewards, a reasonable interest rate, and clear terms. If you have no credit history, consider starting with a secured credit card.

Most importantly, use your card responsibly. Pay on time, keep your balance low, and avoid spending money you do not have.

A credit card is not just a spending tool. When used carefully, it can become a useful part of your financial foundation.

Disclaimer: This article is for educational purposes only and should not be considered financial, legal, tax, or investment advice. Always review official product terms and consider speaking with a qualified professional before making financial decisions.

Disclaimer

This article is for educational purposes only and should not be considered financial, legal, tax, credit, or investment advice. Always review official product terms before applying for any credit card.

Leave a Reply