Saving money is an important part of personal finance, but it does not always mean making big changes. For many people, saving starts with small everyday decisions.

A few dollars saved here and there may not seem like much at first. But over time, small savings can help you build an emergency fund, reduce debt, prepare for future expenses, and feel more in control of your money.

For beginners, the goal is not to stop spending completely. The goal is to understand where your money goes and make better choices.

This guide shares practical saving money tips for everyday Americans.

Why Saving Money Matters

Saving money matters because it gives you more financial flexibility.

Without savings, unexpected expenses can quickly create stress. A car repair, medical bill, home repair, or income change may force you to use credit cards, loans, or borrowed money.

Savings can help you:

- Prepare for emergencies

- Avoid unnecessary debt

- Pay for future goals

- Reduce financial stress

- Handle irregular expenses

- Feel more confident with money

- Build better financial habits

Even a small amount of savings can make a difference.

If you save consistently, your money can grow over time.

Start With a Simple Budget

A budget helps you understand your income and expenses.

Without a budget, it is easy to spend money without realizing where it went.

Start by writing down your monthly take-home income. Then list your regular expenses, such as rent, utilities, groceries, transportation, insurance, phone bill, debt payments, and subscriptions.

After that, look at flexible spending, such as restaurants, entertainment, shopping, hobbies, and delivery apps.

A simple budget helps you see what is necessary and what can be adjusted.

Your budget does not need to be perfect. It only needs to give your money a plan.

Track Where Your Money Goes

Before you can save more, you need to know where your money is going.

Review your bank account, debit card, credit card, and payment app transactions.

Look at the last 30 days and group your spending into categories.

Common categories include:

- Housing

- Utilities

- Groceries

- Transportation

- Restaurants

- Subscriptions

- Shopping

- Insurance

- Debt payments

- Savings

- Entertainment

- Personal care

Tracking spending can show patterns you may not notice.

For example, you may discover that small daily purchases are costing more than expected.

Once you know your patterns, it becomes easier to make changes.

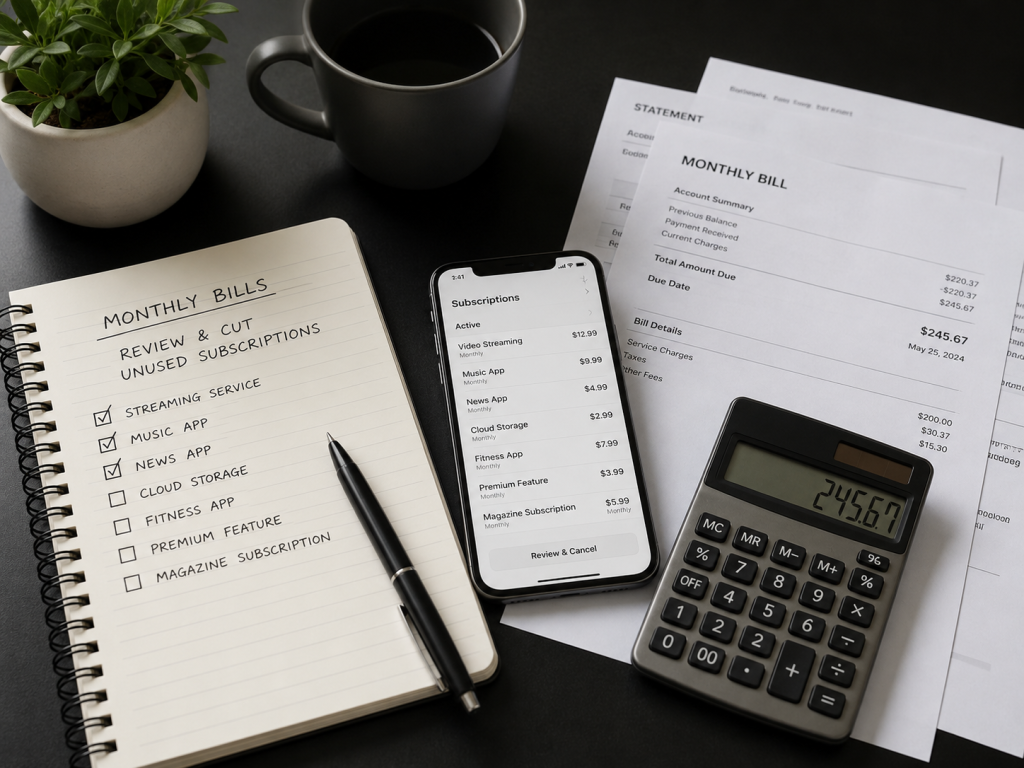

Cut Unused Subscriptions

Subscriptions are one of the easiest places to save money.

Many people pay for services they rarely use.

Common subscriptions may include streaming apps, music apps, cloud storage, fitness apps, shopping memberships, software tools, meal delivery memberships, and mobile apps.

Review your statements and look for recurring charges.

Ask yourself:

- Do I still use this service?

- Is it worth the monthly cost?

- Can I cancel it?

- Can I switch to a cheaper plan?

- Can I share a plan legally with family?

- Can I pause it for a few months?

Canceling even one or two unused subscriptions can free up money without changing your daily life very much.

Reduce Food and Takeout Spending

Food is a major spending category for many households.

Groceries are necessary, but takeout, delivery fees, restaurant meals, and impulse snacks can add up quickly.

You do not need to stop eating out completely. But reducing how often you order food can help you save money.

Simple ways to reduce food spending include:

- Plan meals before grocery shopping

- Use a shopping list

- Cook simple meals at home

- Bring lunch to work

- Limit delivery apps

- Compare grocery prices

- Use leftovers

- Avoid shopping when hungry

- Buy basic ingredients instead of convenience foods

Small changes in food spending can create noticeable savings over a month.

Compare Phone, Internet, and Insurance Bills

Many people keep the same phone, internet, or insurance plan for years without comparing options.

Over time, you may be paying more than necessary.

Review your monthly bills and ask whether the plan still fits your needs.

You can compare:

- Phone plans

- Internet plans

- Car insurance

- Renters insurance

- Home insurance

- Streaming bundles

- Utility providers where available

Sometimes a lower-cost plan may provide enough service.

You can also contact the company and ask whether there are lower plans, promotions, or discounts.

Do not reduce important coverage without understanding the risk. But it is worth checking whether you are paying for features you do not use.

Use a Shopping List

A shopping list is a simple tool that can help reduce impulse spending.

Before going to the store or shopping online, write down what you actually need.

Then try to stick to the list.

This works for groceries, household items, clothing, and personal care products.

Without a list, it is easy to buy extra items because they look useful in the moment.

A shopping list helps you stay focused and avoid buying things you already have at home.

For online shopping, try keeping items in your cart for 24 hours before buying. This gives you time to decide whether the purchase is truly necessary.

Avoid Impulse Purchases

Impulse purchases can quietly damage a budget.

An impulse purchase is something you buy without planning.

It may happen because of stress, boredom, advertising, discounts, social media, or convenience.

To reduce impulse purchases, try these habits:

- Wait 24 hours before buying non-essential items

- Unsubscribe from promotional emails

- Remove saved card details from shopping websites

- Avoid browsing shopping apps when bored

- Set a monthly fun-money limit

- Compare prices before buying

- Ask whether the item solves a real need

The goal is not to remove all enjoyment.

The goal is to spend intentionally instead of automatically.

Build an Emergency Fund

An emergency fund is money saved for unexpected expenses.

This is one of the most important saving goals for beginners.

Unexpected costs can happen at any time. If you do not have savings, you may need to rely on credit cards or loans.

Start with a small goal, such as $500 or $1,000.

This can help cover smaller emergencies, such as minor car repairs, medical costs, or urgent bills.

After reaching a starter goal, you can work toward saving several months of essential expenses.

Keep your emergency fund separate from daily spending money so it is not easy to use for non-emergencies.

Save Automatically When Possible

Automatic savings can make saving easier.

Instead of waiting to see what is left at the end of the month, you can move money into savings shortly after you get paid.

This can be done through automatic transfers from checking to savings.

The amount does not have to be large.

You might start with $10, $25, $50, or $100 per paycheck.

The habit matters more than the amount.

Automatic savings can help you stay consistent because you do not have to remember every time.

If your income changes, you can adjust the amount.

Lower Energy and Utility Costs

Utility bills can be another area where small habits help.

Simple ways to reduce energy costs may include turning off lights, unplugging unused devices, using energy-efficient bulbs, adjusting the thermostat, washing clothes with cold water, and reducing unnecessary water use.

These changes may not save a huge amount immediately, but they can help lower monthly expenses over time.

It is also helpful to review utility bills and understand seasonal changes.

Some months may naturally be higher because of heating or cooling costs.

Planning ahead can help avoid surprises.

Buy Used When It Makes Sense

Buying used can save money on many items.

Examples include furniture, tools, books, clothing, small appliances, sports equipment, and household items.

Not everything should be bought used, but many everyday items do not need to be brand new.

Before buying something new, check whether a good used option is available.

However, be careful with safety-related items, electronics without warranties, or products that may have hidden damage.

The goal is to save money without creating bigger problems later.

Plan for Irregular Expenses

Some expenses do not happen every month, but they still happen.

Examples include car registration, annual insurance, holiday gifts, school supplies, birthdays, repairs, tax preparation, and medical appointments.

If you do not plan for these, they can feel like emergencies.

A simple method is to estimate the yearly cost and divide it by 12.

For example, if you expect to spend $600 on holiday gifts, saving $50 per month can make that expense easier to handle.

Planning for irregular expenses can reduce stress and protect your emergency fund.

Use Cash Back and Rewards Carefully

Cash back and rewards can be useful, but only if you use them carefully.

Do not spend extra money just to earn rewards.

For example, earning 2 percent cash back does not help if you buy things you did not need.

If you use a credit card, try to pay the full statement balance on time to avoid interest.

Interest charges can quickly erase any rewards earned.

Rewards should be a small benefit, not the reason for overspending.

Common Money-Saving Mistakes

One common mistake is trying to cut too much at once.

If your plan feels too strict, it may be hard to follow.

Another mistake is ignoring small expenses. Small purchases can add up over time.

Some beginners save money but keep it in the same account as spending money. This makes it easier to use by accident.

Another mistake is focusing only on discounts. Buying something on sale still costs money if you did not need it.

Some people also forget to plan for irregular expenses.

Saving money works best when your plan is realistic and consistent.

Final Thoughts

Saving money does not always require a major lifestyle change.

For everyday Americans, small practical habits can make a real difference.

Start with a simple budget. Track your spending. Cancel unused subscriptions. Reduce takeout. Compare bills. Use shopping lists. Avoid impulse purchases. Build an emergency fund. Save automatically when possible.

The goal is not to be perfect.

The goal is to make steady progress and build better money habits over time.

Even small savings can help you feel more prepared, reduce stress, and create more financial flexibility.

Disclaimer

The information in this article is for educational purposes only and should not be considered financial, legal, tax, credit, loan, or investment advice. Saving strategies, budgeting methods, and financial decisions may not fit every personal situation. Always review your own income, expenses, obligations, and financial needs before making financial decisions. If you have questions about your personal financial situation, consider speaking with a qualified professional.

Leave a Reply