Loan reviews can be helpful when you are comparing personal loans, auto loans, student loans, or other borrowing options.

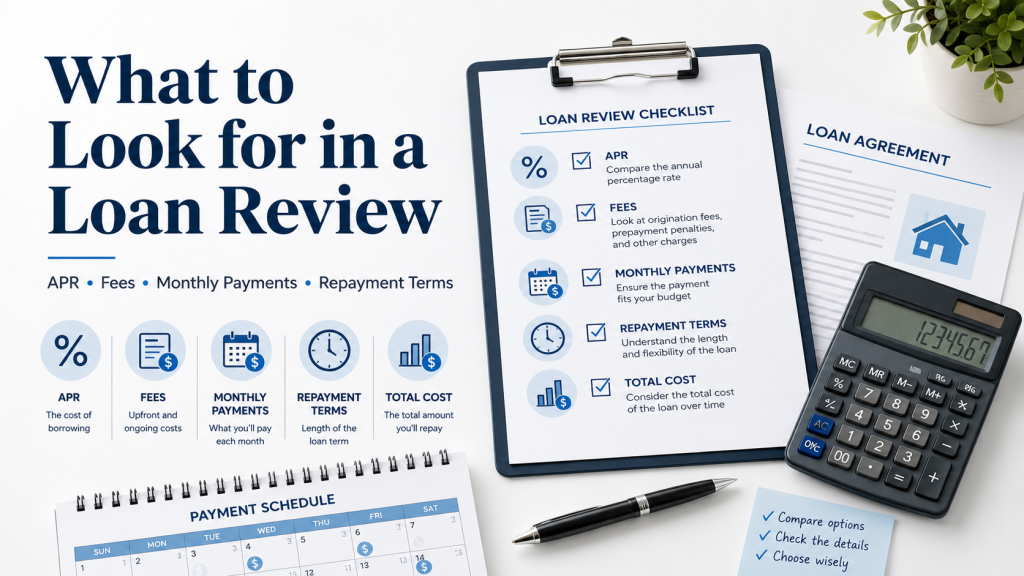

A loan review may explain APR, fees, monthly payments, repayment terms, lender requirements, risks, and total cost.

However, beginners should not choose a loan only because a review sounds positive or because the monthly payment looks low.

A good loan review should help you understand the full cost of borrowing and whether the loan fits your budget.

This guide explains what beginners should look for when reading a loan review.

Why Loan Reviews Matter

Loan reviews matter because loans can affect your monthly budget, credit history, debt level, and long-term financial situation.

A loan may help pay for a large expense, consolidate debt, repair a vehicle, cover emergency costs, or finance another important need.

But loans also create repayment responsibility.

If the loan has a high APR, expensive fees, long repayment term, or payment that does not fit your budget, it can become stressful.

A good loan review should explain:

- What the loan is for

- Who the loan may fit

- What APR applies

- What fees may be charged

- How repayment works

- What the monthly payment may be

- What the total cost may be

- What requirements apply

- What risks exist

- What alternatives may be available

For beginners, the goal is to understand the full picture before applying.

Understand the Loan Purpose

Before comparing loan reviews, understand the purpose of the loan.

Different loans are designed for different needs.

A personal loan may be used for debt consolidation, home repairs, medical bills, large purchases, or emergency expenses.

An auto loan is usually used to buy a vehicle.

A student loan is usually used for education expenses.

A mortgage is used to buy a home.

The purpose matters because loan terms, rates, repayment schedules, and requirements can be different.

Before applying, ask:

- Why do I need this loan?

- Is borrowing necessary?

- Can I wait and save instead?

- Will this loan improve my situation?

- Can I repay it comfortably?

- Is there a lower-cost option?

A loan should solve a real problem, not create a bigger one.

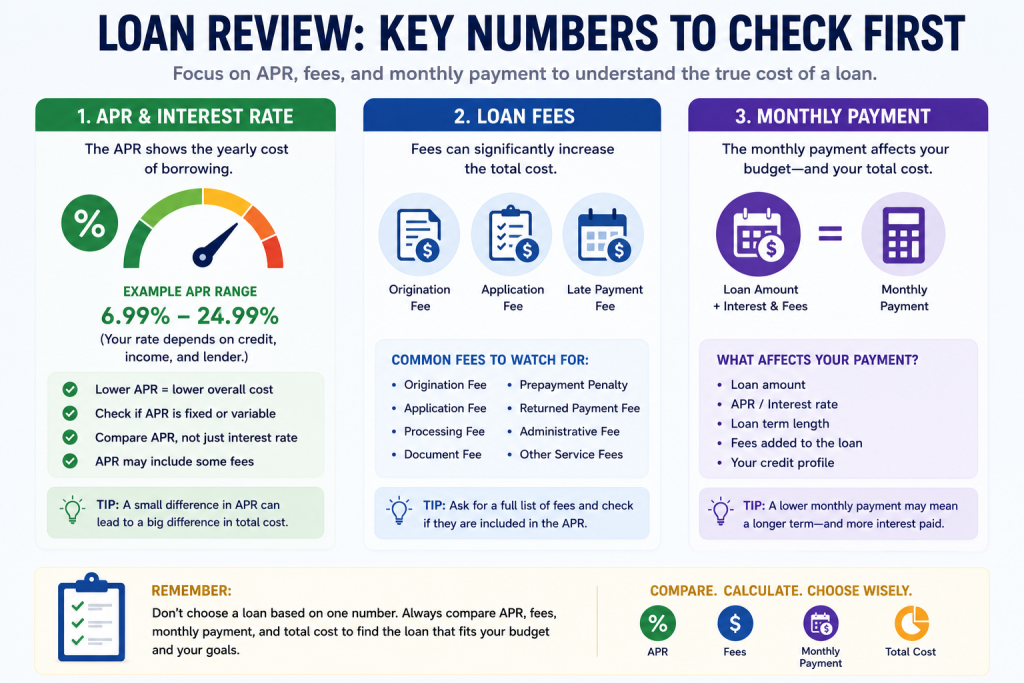

Check APR and Interest Rate

APR is one of the most important things to check in a loan review.

APR stands for Annual Percentage Rate.

APR helps show the yearly cost of borrowing money, including the interest rate and certain fees.

The interest rate is the cost charged for borrowing the loan amount.

APR may give a broader view of the total borrowing cost.

A good loan review should explain:

- Advertised APR range

- Estimated APR

- Whether the APR is fixed or variable

- How APR affects monthly payments

- How APR affects total repayment cost

- Whether fees are included in APR

- Whether rates depend on credit and income

A lower APR usually means lower borrowing cost, but APR is not the only factor.

You should also review fees, repayment term, monthly payment, and total cost.

Review Loan Fees

Loan fees can increase the real cost of borrowing.

Some loans have few fees, while others may include several charges.

Common loan fees may include:

- Origination fee

- Application fee

- Late payment fee

- Returned payment fee

- Prepayment penalty

- Administrative fee

- Processing fee

- Document fee

- Service fee

An origination fee is a fee some lenders charge for processing the loan.

It may be deducted from the loan amount or added to the cost.

For example, if you borrow $5,000 and there is an origination fee, you may receive less than the full amount or pay more overall.

Before applying, ask:

- What fees apply?

- When are fees charged?

- Can fees be avoided?

- Are fees included in the APR?

- Will the fees reduce the amount I receive?

- Are there cheaper options?

A loan with a low interest rate but high fees may not be the best choice.

Compare Monthly Payments

Monthly payment is important because it affects your budget.

A loan review should explain the estimated monthly payment and how it is calculated.

However, beginners should not choose a loan only because the monthly payment is low.

A low monthly payment may come from a longer repayment term.

A longer term can make the payment easier each month, but it may increase the total interest paid over time.

Before choosing a loan, ask:

- Can I afford the monthly payment?

- Will the payment fit my budget?

- What happens if my income changes?

- Does the payment include fees?

- How many months will I pay?

- Will a shorter term save money?

The best monthly payment is not always the lowest one.

It should be affordable while keeping the total cost reasonable.

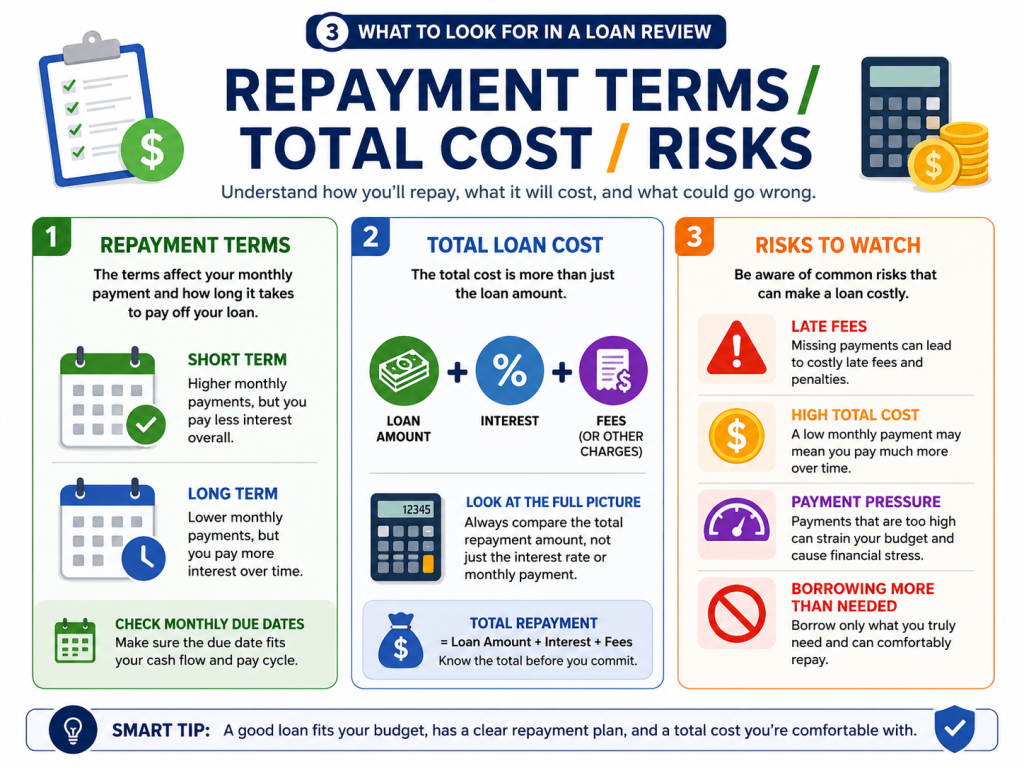

Understand Repayment Terms

Repayment terms explain how long you will repay the loan and how payments work.

For example, a loan may have a repayment term of 12 months, 24 months, 36 months, 60 months, or longer.

A review should explain:

- Loan term length

- Monthly payment schedule

- Due date rules

- Payment methods

- Autopay options

- Late payment rules

- Grace period

- Prepayment rules

- Payoff options

A shorter repayment term usually means higher monthly payments but lower total interest.

A longer repayment term usually means lower monthly payments but higher total interest.

Before accepting a loan, make sure you understand the repayment schedule clearly.

Look at Total Loan Cost

Total loan cost is one of the most important parts of a loan review.

The total loan cost includes the amount borrowed, interest, and fees.

A loan may look affordable if you only focus on the monthly payment, but the total cost may be much higher over time.

A good review should help you understand:

- Loan amount

- Interest cost

- Fees

- Monthly payment

- Repayment term

- Total repayment amount

For example, two loans may have the same loan amount but different APRs and repayment terms.

The loan with the lower monthly payment may not always be cheaper.

Always compare the total amount you will repay.

Check Lender Requirements

Different lenders have different requirements.

A loan review should explain what borrowers may need to qualify.

Common requirements may include:

- Credit score review

- Income verification

- Employment information

- Debt-to-income review

- Identity verification

- Bank account information

- Collateral

- Minimum loan amount

- Maximum loan amount

- Residency requirements

Some lenders may offer loans for borrowers with strong credit.

Others may work with borrowers who have limited or fair credit, but the APR may be higher.

Before applying, check whether you are likely to meet the requirements.

Also check whether the application may involve a hard credit inquiry.

Review Risks and Limitations

A balanced loan review should explain risks and limitations.

Loans can be useful, but they also create debt.

Common risks may include:

- High APR

- Expensive fees

- Long repayment terms

- Monthly payment pressure

- Late payment fees

- Credit score impact

- Debt cycle risk

- Prepayment penalties

- Collateral loss for secured loans

- Borrowing more than needed

If a loan is secured, it may require collateral.

Collateral is something valuable used to support the loan, such as a vehicle or property.

If payments are not made, the lender may have rights connected to the collateral depending on the loan terms.

Beginners should understand the risks before borrowing.

Compare the Loan With Other Options

One loan review is not enough.

It is better to compare multiple options before applying.

Compare:

- APR

- Interest rate

- Origination fee

- Monthly payment

- Loan term

- Total repayment cost

- Late fees

- Prepayment rules

- Lender requirements

- Customer support

- Funding speed

- Loan limits

- Borrower reviews

You may also compare the loan with other choices, such as saving first, using emergency savings, negotiating a bill, or choosing a lower-cost alternative.

Borrowing should be a thoughtful decision, not a rushed one.

Review Customer Support

Customer support is important when choosing a lender.

You may need help with payments, account access, payoff information, due date questions, late payment issues, or loan documents.

A loan review should consider whether customer support is easy to reach.

Look for:

- Phone support

- Email support

- Live chat

- Secure messaging

- Help center articles

- Support hours

- Payment assistance options

- Clear payoff instructions

Poor customer support can make a loan more stressful if problems happen.

Read the Official Loan Terms

Loan reviews are useful, but the official loan terms are more important.

Before accepting any loan, read the official loan agreement and disclosures carefully.

Check:

- APR

- Interest rate

- Loan amount

- Monthly payment

- Repayment term

- Total repayment amount

- Fees

- Due dates

- Late payment rules

- Prepayment rules

- Autopay terms

- Collateral terms

- Default rules

- Cancellation rights if applicable

Do not rely only on a review, advertisement, or estimated payment.

The official agreement controls the real loan terms.

Common Beginner Mistakes

One common mistake is choosing a loan only because the monthly payment is low.

A low monthly payment may result in a higher total cost over time.

Another mistake is ignoring origination fees or other charges.

Some beginners focus on the loan amount but forget to calculate the total repayment amount.

Others apply before checking requirements.

Another mistake is borrowing more than needed.

Some people also ignore late payment rules or prepayment penalties.

A good loan review should help beginners avoid these mistakes.

Simple Checklist Before Applying

Before applying for a loan, ask:

- Why do I need this loan?

- Is borrowing necessary?

- What is the APR?

- What is the interest rate?

- What fees apply?

- What is the monthly payment?

- Can I afford the payment?

- How long is the repayment term?

- What is the total repayment cost?

- Are there prepayment penalties?

- What requirements apply?

- Will the lender run a hard credit check?

- What happens if I miss a payment?

- Have I compared other options?

- Have I read the official loan agreement?

If you cannot answer these questions, take more time before applying.

Final Thoughts

Loan reviews can help beginners compare borrowing options more clearly.

A good loan review should explain APR, interest rates, fees, monthly payments, repayment terms, total loan cost, lender requirements, customer support, risks, and limitations.

Do not choose a loan only because it has fast approval or a low monthly payment.

Look at the full cost and make sure the payment fits your budget.

For beginners, the best loan is usually one that is clear, affordable, realistic, and easy to understand.

Always review the official loan agreement before accepting any loan.

Disclaimer

The information in this article is for educational purposes only and should not be considered financial, legal, tax, credit, banking, loan, or investment advice. Loan APRs, interest rates, fees, repayment terms, approval requirements, lender policies, and borrower protections may change over time. Always review the official loan agreement, rates, fees, repayment terms, and disclosures from the lender before applying for or accepting any loan. If you have questions about your personal financial situation, consider speaking with a qualified professional.

Leave a Reply